The AI arms race isn’t just about cloud servers and chatbots anymore; it’s spilling into the physical world. Companies like Nvidia (NVDA) are now pushing “physical AI” for robots and automation. Robots that see, move, and think are on the rise, and chipmakers want a piece of that action.

That’s where STMicroelectronics (STM) comes into the picture. Earlier this week, ST announced an expanded partnership with Nvidia to fast-track “physical AI” systems. The deal means ST’s sensors, microcontrollers, and motor-control chips will be integrated into Nvidia’s robotics platforms like Isaac Sim, Holoscan, and Jetson to simplify building humanoid and industrial robots.

With Nvidia’s CEO calling this the “ChatGPT moment for robotics,” ST is positioning itself as a key supplier. Let's break down what that could mean for STMicro and its stock.

STM Builds AI Capabilities

STMicroelectronics is a Swiss-based global semiconductor leader. It makes a wide range of chips from microcontrollers and sensors to power ICs and analog devices. Its chips are used in everything from cars and factory equipment to smartphones and IoT gadgets. ST’s portfolio spans the “things” of tech, giving it a unique play on both automotive electronics and emerging areas like industrial IoT and now robotics.

STMicroelectronics isn’t just betting on physical AI; it’s building across multiple fronts. Recently. It launched a new ultra-wideband chip, pushing deeper into smart sensing for cars and devices. It’s also scaling silicon photonics for AI data centers. And now, ST is deploying over 100 robots in its older fabs to handle repetitive wafer-handling tasks. The idea is to boost efficiency and retrain staff for higher-skilled roles, avoiding plant closures. ST’s manufacturing head said one humanoid could replace three of four shifts. This shows it’s not just enabling automation but using it too.

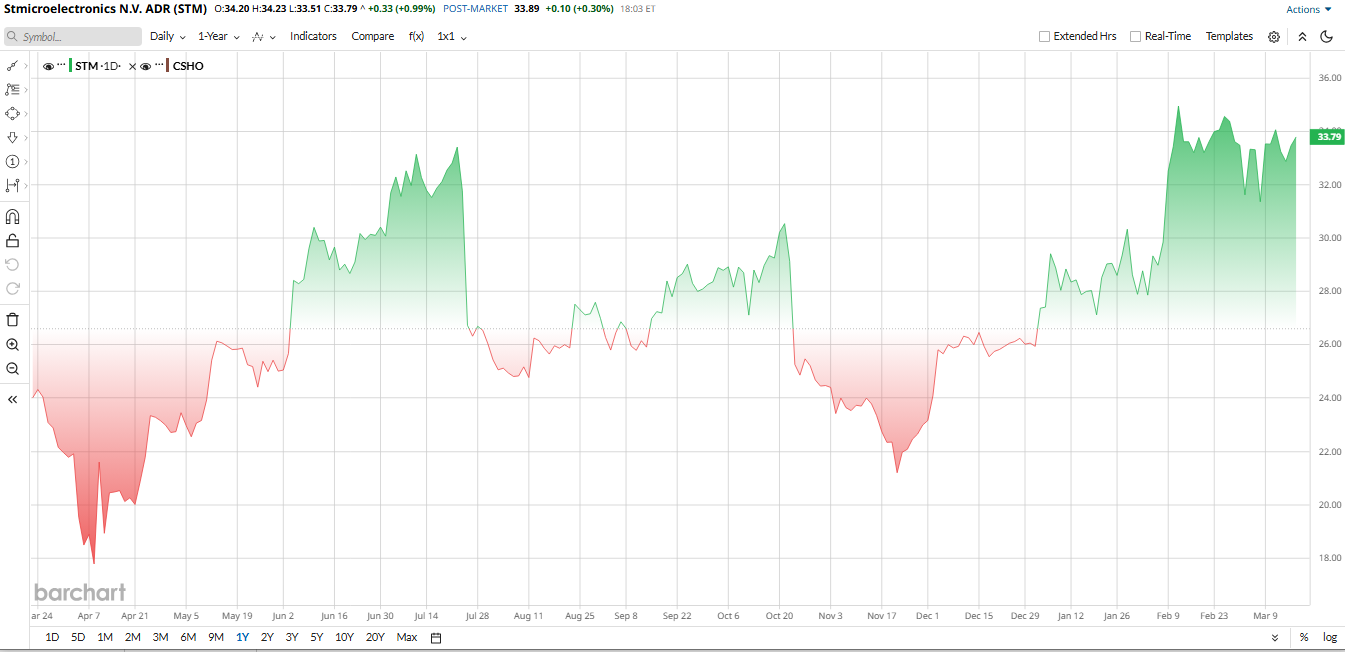

Valued at $13 billion by market cap, STM stock has bounced back strongly in the last year. The shares delivered a roughly 31% total return over the past 12 months and are up about 30% year-to-date (YTD). This outpaced many chip peers, helped by recovering auto/industrial demand and the recent AI buzz.

However, this run-up means valuations are getting rich. STM’s forward EV/EBITDA is about 9.2×, which is high by its own historical standards; its three-year median was 5.7×. Its forward P/E is roughly 34×, versus the semiconductor sector’s mid-20s range. So we can say that STM trades at a premium to history and modestly above peers. The market is clearly pricing in growth, but there isn’t much margin of safety at current levels.

Nvidia Tie-In: A Physical AI Partnership

The big news is the Nvidia collaboration. On March 16, ST announced it will integrate its sensors, STM32 microcontrollers, and motor drivers into Nvidia’s robotics ecosystem. For example, ST’s Leopard Imaging stereo depth camera is being added to Nvidia’s Holoscan Sensor Bridge, and ST’s high-fidelity IMU model is now part of the Isaac Sim virtual training suite. ST’s own executives frame this as a major step. SVP Rino Peruzzi said the goal is to “unleash the next wave of cutting-edge robotics innovation” by making it easier to plug ST hardware into Nvidia’s platforms. In practical terms, it means robotics developers can connect STM32 chips, advanced sensors, and motors to Nvidia’s Jetson AI modules via pre-built software bridges.

ST Beats Revenue, Yet Misses Earnings Estimate

Latest financials support the ST rally story, yet profitability remains an issue. In Q4, ST reported $3.33 billion in revenue, above its guidance range, and this quarter marked ST’s first year-over-year (YoY) growth in some time. CEO Jean-Marc Chery noted that strong demand in Personal Electronics and Consumer/Industrial chips offset weakness in Automotive.

On the earnings side, EPS came short of estimates and had a small net loss of $0.03 per share because of one-time items. Despite this, management pointed out that Q4 performance “returned to year-over-year growth” after several down quarters. Plus, the company invested heavily in about $1.79 billion in capex and still generated $265 million in free cash flow.

Looking ahead, ST gave Q1 2026 guidance of $3.04 billion in revenue, which is down about 8.7% sequentially but still implies accelerating year-on-year growth. Gross margin is seen around 33.7%. Analysts expect ST to capitalize on these trends. Consensus estimates from stockanalysis.com suggest 2026 revenue of $13.7 billion versus $11.8 billion last year and adjusted EPS of roughly $1.22 compared to $0.18 prior, reflecting a rebound in key markets.

During the earnings call, CEO Chery remains cautiously optimistic. He emphasized investing in R&D and production capacity to serve automotive and AI-enabled applications. “Our Q1 outlook accelerates the year-over-year growth dynamic that started in Q4,” he said, hinting that ST expects momentum to continue. The key will be execution: hitting guidance and managing costs.

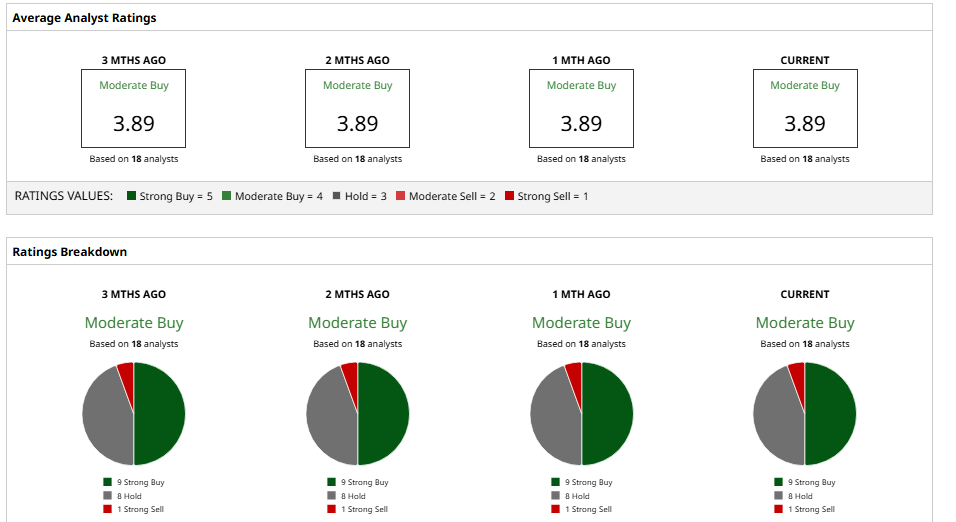

What Is Wall Street's Take on STM Stock?

Wall Street’s opinion on STM stock is generally positive, evidenced by their consensus “Moderate Buy” rating. The consensus 12-month price target is only around $34, roughly flat to slightly below the current price. However, the street high target of $45 still implies an expected 32% upside.

In separate terms, Susquehanna’s Chris Rolland remains bullish; he just raised his STM target to $40 from $35. Rolland notes industrial and auto demand rebounding in 2026, plus new markets like AI, LEO satellites, and “800V DC” data-center power solutions. He points specifically to opportunities in humanoid robotics and silicon photonics. In his view, these factors justify ST’s growth story.

Others are a little more cautious. So the conclusion is that the Street isn’t overwhelmingly enthusiastic. As one analyst note put it, ST is “good but not great” solid tech, but the stock already reflects much of its potential. Ultimately, analysts say STM’s risk/reward hinges on execution. If physical AI and other new businesses deliver, STM’s premium valuation can be earned; if not, the stock could stall.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Add Global Exposure to Your Portfolio with This 1 Norwegian ETF

- Meta Could Cut 20% of Its Jobs as AI Costs Pile Up. Should You Buy, Sell, or Hold META Stock Before Layoffs?

- Dear Tesla Stock Fans, Mark Your Calendars for March 21

- Disney Gets a New Executive Team As 'Iger Era' Ends: Does That Make DIS Stock a Buy?