Block (XYZ) stock has suddenly grabbed all attention on the Street. Shares of the fintech company behind Square and Cash App shocked the market after soaring roughly 20% following a massive wave of AI-driven layoffs announced by CEO Jack Dorsey. The move of cutting around 4,000 employees, nearly 40% of the company’s workforce, is one of the boldest corporate bets yet on how artificial intelligence (AI) is reshaping how companies operate. Now the question is whether this rally is the start of a new growth phase or just a short-term bounce.

Should you buy, hold, or dump XYZ stock now?

Why Block's Stock Suddenly Jumped

The market loves efficiency. Block's stock is down 14% in the past six months and is flat so far this year. However, the recent 25% rally over the last five days suggests that investors are increasingly rewarding companies that promise automation, efficiency, and leaner operations.

During the Q4 earnings call, management emphasized that some engineering projects that previously took weeks to complete can now be done much faster with AI-assisted coding tools. Layoffs often signal cost discipline and margin expansion, and the company stressed that it is doing so not from a position of weakness. By cutting thousands of jobs, Block could dramatically reduce operating expenses while maintaining or even increasing output through AI tools.

AI Tools Are Already Changing Productivity

In the fourth quarter, Block’s gross profit increased 24% year-over-year (YoY) to $2.87 billion, while adjusted diluted earnings per share rose 38% YoY. For the full year 2025, Block reported $10.36 billion in gross profit, marking 17% annual growth. The company also repurchased $790 million worth of shares in the fourth quarter alone, bringing total buybacks for 2025 to $2.3 billion.

Management now expects gross profit to increase 18% YoY to $12.2 billion along with 54% growth in adjusted operating income. Additionally, adjusted diluted earnings per share are expected to rise by 54% to $3.66 in 2026. These projections imply that a combination of strong revenue growth and a lower cost base could significantly expand margins in the coming years.

Block’s largest ecosystems, Cash App and Square, continue to be key pillars of its ongoing success. Notably, Cash App monthly active users climbed to 59 million by the end of 2025, while primary banking active users grew 22% YoY to 9.3 million. Meanwhile, Square's gross payment volume growth accelerated to 10% in 2025, and the company reported its strongest year ever for new seller volume added. Block has spent the past several years investing in internal automation systems and AI infrastructure. Some of these tools have already been fully implemented, while others are still being developed. Management believes the benefits will be more substantial when the technology improves. Block’s vision is to eventually become a “smaller, faster, intelligence-native company.”

The consensus estimates for Block’s earnings for 2026 are $3.55, which is lower than management’s projections. It represents earnings growth of 49.7%, followed by another 30.8% in 2027. Trading at 17 times forward earnings, Block looks cheap for a fintech stock delivering that level of growth. However, whether the valuation will ultimately depend on whether the company’s restructuring and AI-driven efficiency plans translate into sustained margin expansion over the coming quarters.

What Does Wall Street Say About XYZ Stock Now?

Even Wall Street appears to be impressed by companies that strive to be more efficient. Intrigued with Block’s decision to cut off the workforce and its strong Q4 results, Oppenheimer increased the stock’s price target to $89 from $85 while retaining an “Outperform” rating on XYZ.

Similarly, HSBC upgraded XYZ stock to a “Buy” from “Hold,” citing that the company's decision to cut jobs came from a position of strength given its excellent financials. The firm also increased the target price for the stock to $77 from $70.

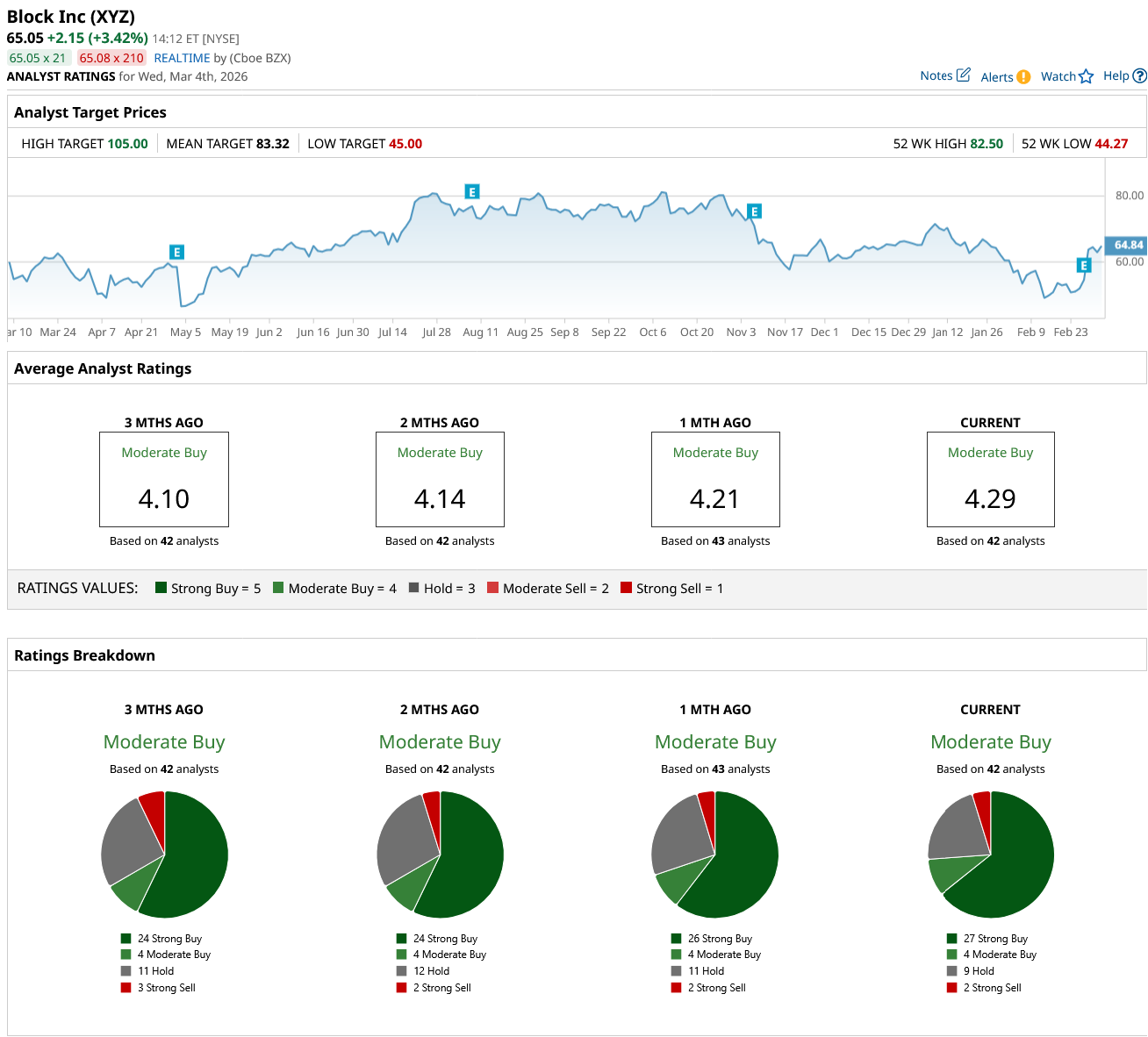

Overall, on Wall Street, XYZ stock is a “Moderate Buy.” Out of the 42 analysts covering the stock, 27 have a “Strong Buy” recommendation, four say it's a “Moderate Buy,” nine rate it a “Hold,” and two suggest a “Strong Sell.” The average price target of $83.32 implies the stock can climb 28% from current levels. Plus, its Street-high price target of $100 suggests an upside of 54% in the next 12 months.

The Bottom Line: It is a Gamble

While Block’s decision seems rewarding now, I feel investors will need to watch closely to see whether the promised productivity gains from AI translate into sustained growth. My concerns are that large workforce reductions and rapid restructuring could disrupt teams, pressurize the existing workforce, and slow down product development in the short term, causing the stock to stay volatile.

If Jack Dorsey’s bold AI strategy succeeds, Block could emerge as a leaner, more profitable fintech powerhouse. In that case, existing investors might want to hold on to the stock. However, if it fails, the rally could end up looking like just another short-lived tech hype. So, conservative investors might consider taking the profits.

For now, one thing is certain: Block’s AI gamble has turned the company into one of the most fascinating fintech stories on Wall Street. Aggressive investors who want to be part of this gamble might want to accumulate shares of this fintech now while it still trades at a discount.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart