Earnings season is moving at full speed, but investors haven’t been handing out easy rewards. Even companies that top Wall Street’s estimates are seeing their stocks tumble if guidance disappoints or management signals heavier near-term spending. In today’s market, a simple earnings beat isn’t enough — investors want strong forecasts, disciplined costs, and clear visibility. Anything less, and the reaction can be swift and unforgiving. That dynamic has been especially brutal for capital-intensive tech names, where heavy AI capital expenditures and elevated guidance have turned upbeat prints into sell-the-news events.

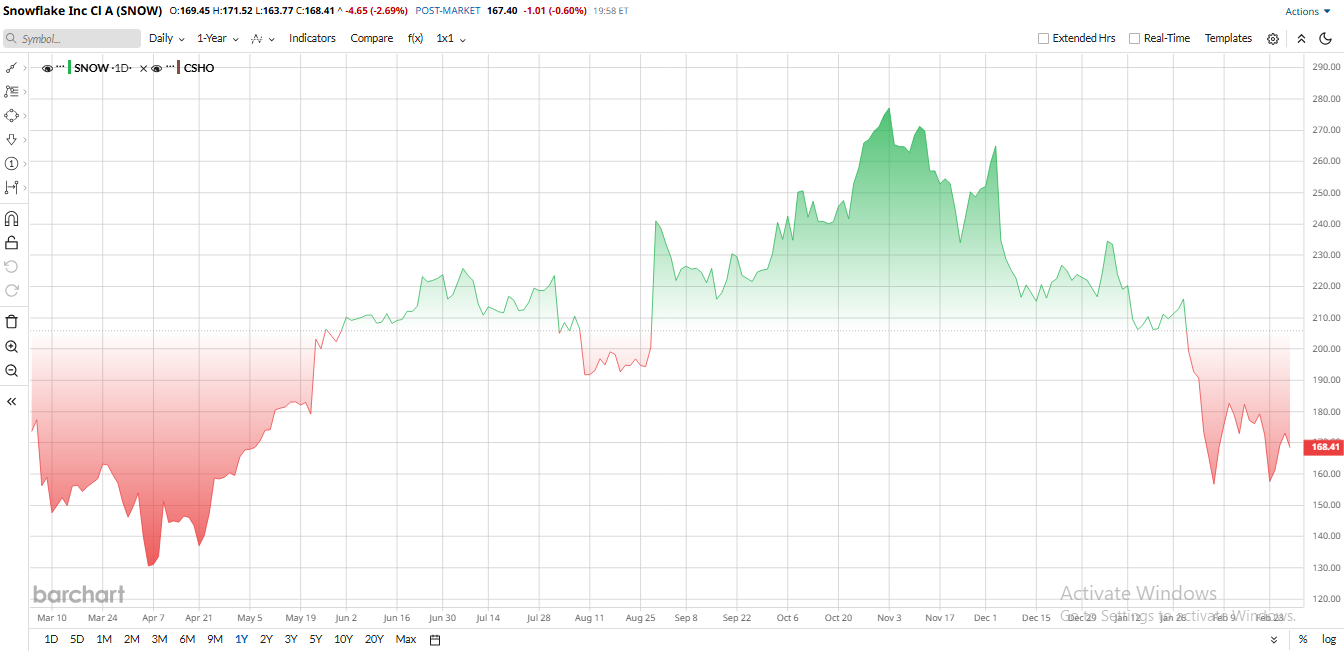

One notable casualty has been Snowflake (SNOW), which has plunged significantly in 2026, and not because of its earnings. Snowflake has been caught in the crossfire of concerns that AI-native architectures and autonomous agents could weaken demand for legacy data workflows. Yet a new analyst note from Evercore ISI paints a different picture, describing Snowflake as one of the most resilient “scaffolding” plays in enterprise AI adoption.

So, with sentiment shaky but fundamentals still intact, the big question for investors is simple: Should you buy the dip in SNOW stock now?

Snowflake Builds Its AI Scaffolding

Founded in 2012, Snowflake is a cloud software company that counts hundreds of Fortune 2000 companies as customers, including many in financial services, media, and retail. Its architecture and “data sharing” features aim to simplify cross-cloud data collaboration while maintaining enterprise-grade security and governance.

Importantly, the company hasn’t been standing still amid the AI disruption debate. Snowflake secured two $200 million multi-year deals, one each with OpenAI and Anthropic, to integrate their cutting-edge AI models into Snowflake's AI Data Cloud. These deals indicate strong enterprise demand for Snowflake’s AI offerings, Snowflake’s new “Cortex” AI services, and reinforce the view that AI workloads drive consumption on its platform.

Additionally, there is news that Snowflake has acquired Observe, bringing observability and monitoring into its portfolio. This acquisition and others — like Tensorstax for AI data engineering — broaden Snowflake’s cloud ecosystem and have been generally viewed as strategic positives.

However, SNOW stock's performance tells a different story. Snowflake started 2026 near the low $200s. Since then, shares have slid roughly 23% on a year-to-date (YTD) basis. This pressure came with the broader “SaaS selloff,” rising interest rates, slowing growth expectations, and a rotation out of richly valued tech names. It also follows late-February headlines and a cautious report from Workday (WDAY), which fueled fears about AI reducing future software spending. In short, the stock drop appears driven more by market mood than by any single company shortfall.

Even after the pullback, valuation remains a central debate. SNOW stock is trading at EV/sales at 12 times and price-to-book ratio at 27.3, significantly higher than the respective sector medians. This suggests Snowflake’s valuation embeds substantial future growth. Wall Street figures the company must continue delivering high 20%-plus revenue growth and improve profit margins to justify this premium. For now, the stock is not “cheap” on metrics — it still ranks among the most richly valued cloud names, implying limited room for error.

Analysts Call the Selloff a Buying Opportunity

Several Wall Street voices argue that the recent pullback in Snowflake looks more like a sentiment-driven reset than a fundamental breakdown. After shares slid alongside the broader AI-linked software cohort, analysts at Citigroup described the move as an overreaction, reiterating confidence in Snowflake’s consumption-based model and long-term AI monetization strategy.

Likewise, commentary from Morgan Stanley emphasized that Snowflake remains a core infrastructure layer for enterprise AI workloads, particularly as companies modernize their data stacks. The firm suggested that while near-term volatility could persist, structural demand for AI-ready data platforms supports sustained high-20% revenue growth.

In short, while traders reacted to macro and AI-spending jitters, several analysts see the dip as a potential entry point rather than a red flag.

Snowflake Delievers Revenue Growth

On Feb. 25, Snowflake reported fourth-quarter results, and the numbers came in stronger than many feared. Revenue rose roughly 30% year-over-year (YOY) to $1.28 billion. The bulk of that, $1.23 billion, came from product revenue tied to its cloud data platform, while about $57 million was generated from professional services and other streams.

Snowflake delivered $0.32 in EPS, comfortably ahead of consensus estimates near $0.27. Free cash flow remained a standout at about $765 million for the quarter, and the company exited the period with roughly $2.83 billion in cash and equivalents, reinforcing balance-sheet strength.

CEO Sridhar Ramaswamy described the quarter as another step forward, noting that Snowflake’s platform “sits at the center of the enterprise AI revolution.” Ramaswamy pointed to growing demand for AI-powered applications layered on top of Snowflake’s data cloud, emphasizing that its decade-long foundation now supports “world-class agentic capabilities.” CFO Brian Robins underscored enterprise traction, highlighting 740 net new customers added during the year and 733 customers now spending over $1 million annually, up 27% YOY.

Looking ahead, management guided for Q1 fiscal 2027 product revenue between $1.262 billion and $1.267 billion, implying about 27% YOY growth. Full-year fiscal 2027 product revenue is expected to reach roughly $5.66 billion, also representing 27% growth. Both figures slightly topped Wall Street’s prior expectations of around $1.23 billion for Q1 and $5.5 billion for the full year.

Wall Street Takes on SNOW Stock

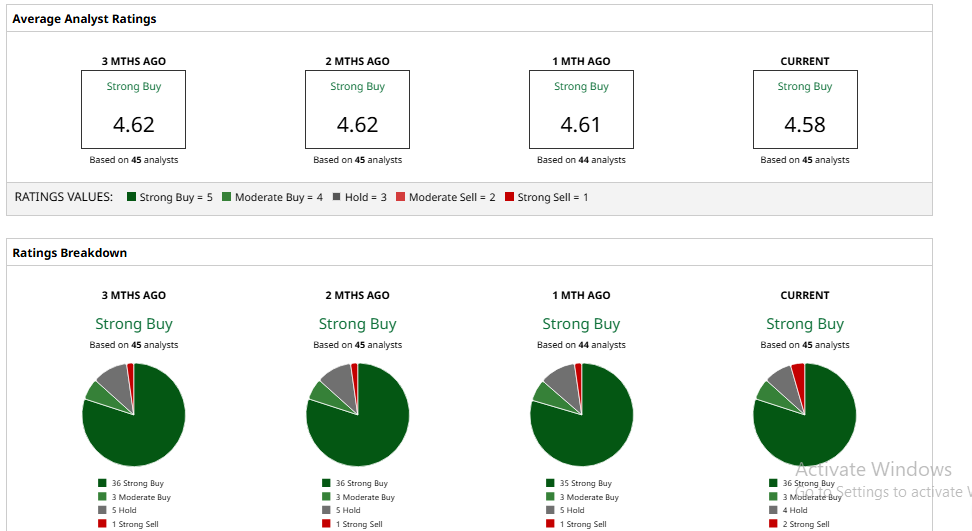

Wall Street is highly confident in Snowflake's growing prospects. Based on 45 analysts with coverage, SNOW stock has a consensus “Strong Buy” rating and a mean price target of $237.26, which implies 40% potential upside from current levels.

In terms of what analysts say, the consistent theme is that Snowflake’s core business is resilient. Citi analyst Tyler Radke explicitly highlighted the company’s “AI-resilient consumption model” and strong traction for Cortex AI. Morgan Stanley’s Keith Weiss pointed out that Snowflake saw the largest acceleration of large-cap software demand in a recent CIO survey.

Overall, analysts acknowledge the high valuation, but many still expect the company to meet its targets and eventually deliver profits, seeing Snowflake as a leader in the AI-driven data cloud.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart