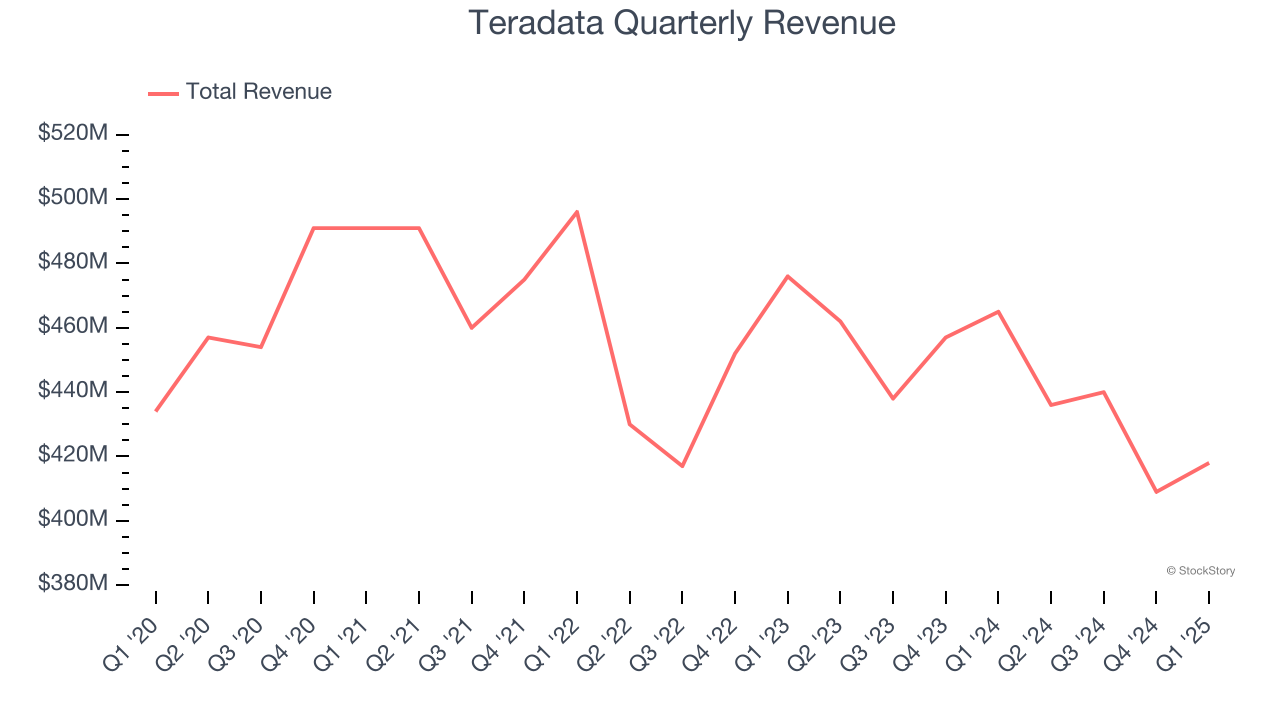

Data and analytics software provider Teradata (NYSE: TDC) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 10.1% year on year to $418 million. Next quarter’s revenue guidance of $401.1 million underwhelmed, coming in 1.9% below analysts’ estimates. Its non-GAAP profit of $0.66 per share was 17% above analysts’ consensus estimates.

Is now the time to buy Teradata? Find out by accessing our full research report, it’s free.

Teradata (TDC) Q1 CY2025 Highlights:

- Revenue: $418 million vs analyst estimates of $428.2 million (10.1% year-on-year decline, 2.4% miss)

- Adjusted EPS: $0.66 vs analyst estimates of $0.56 (17% beat)

- Adjusted Operating Income: $91 million vs analyst estimates of $82.32 million (21.8% margin, 10.6% beat)

- Revenue Guidance for Q2 CY2025 is $401.1 million at the midpoint, below analyst estimates of $409 million

- Management reiterated its full-year Adjusted EPS guidance of $2.20 at the midpoint

- Operating Margin: 15.8%, up from 10.3% in the same quarter last year

- Free Cash Flow Margin: 1.7%, down from 36.2% in the previous quarter

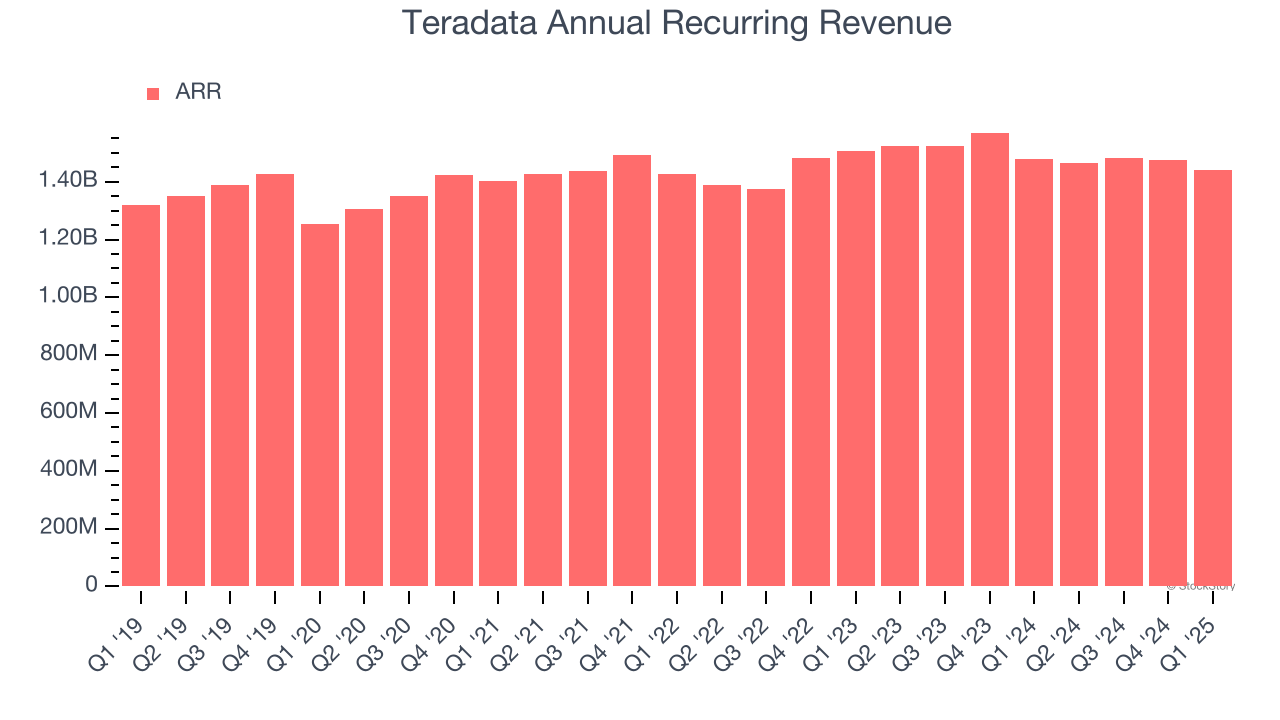

- Annual Recurring Revenue: $1.44 billion at quarter end, down 2.6% year on year

- Market Capitalization: $2.12 billion

“Teradata met our outlook for all key metrics in the first quarter as a result of disciplined execution, continued pull through of the go-to-market actions taken last year and accelerating innovation,” said Steve McMillan, Teradata president and CEO.

Company Overview

Part of point-of-sale and ATM company NCR from 1991 to 2007, Teradata (NYSE: TDC) offers a software-as-service platform that helps organizations manage and analyze their data across multiple storages.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Teradata’s demand was weak over the last three years as its sales fell at a 4% annual rate. This wasn’t a great result and is a sign of poor business quality.

This quarter, Teradata missed Wall Street’s estimates and reported a rather uninspiring 10.1% year-on-year revenue decline, generating $418 million of revenue. Company management is currently guiding for a 8% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 3.3% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and implies its newer products and services will not accelerate its top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Teradata’s ARR came in at $1.44 billion in Q1, and it averaged 3.8% year-on-year declines over the last four quarters. However, this alternate topline metric outperformed its total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Teradata does a decent job acquiring new customers, and its CAC payback period checked in at 47.2 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

Key Takeaways from Teradata’s Q1 Results

It was good to see Teradata provide full-year EPS guidance that slightly beat analysts’ expectations. We were also happy its annual recurring revenue narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed significantly and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 4.3% to $21 immediately following the results.

Teradata didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.