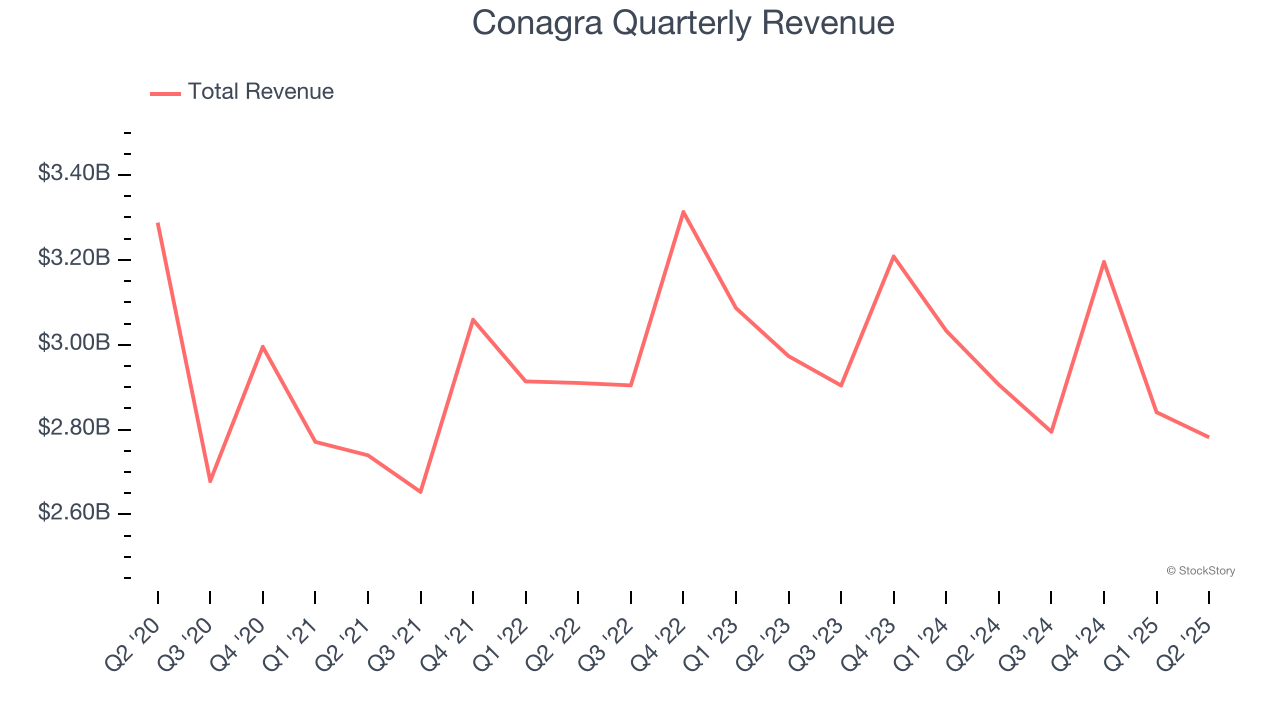

Packaged foods company Conagra Brands (NYSE: CAG) missed Wall Street’s revenue expectations in Q2 CY2025, with sales falling 4.3% year on year to $2.78 billion. Its non-GAAP profit of $0.56 per share was 8.2% below analysts’ consensus estimates.

Is now the time to buy Conagra? Find out by accessing our full research report, it’s free.

Conagra (CAG) Q2 CY2025 Highlights:

- Revenue: $2.78 billion vs analyst estimates of $2.83 billion (4.3% year-on-year decline, 1.7% miss)

- Adjusted EPS: $0.56 vs analyst expectations of $0.61 (8.2% miss)

- Adjusted EBITDA: $544 million vs analyst estimates of $511.5 million (19.6% margin, 6.4% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.78 at the midpoint, missing analyst estimates by 27.6%

- Operating Margin: 11.5%, up from -19.1% in the same quarter last year

- Free Cash Flow Margin: 60.8%, up from 14% in the same quarter last year

- Organic Revenue fell 4.3% year on year (-2.4% in the same quarter last year)

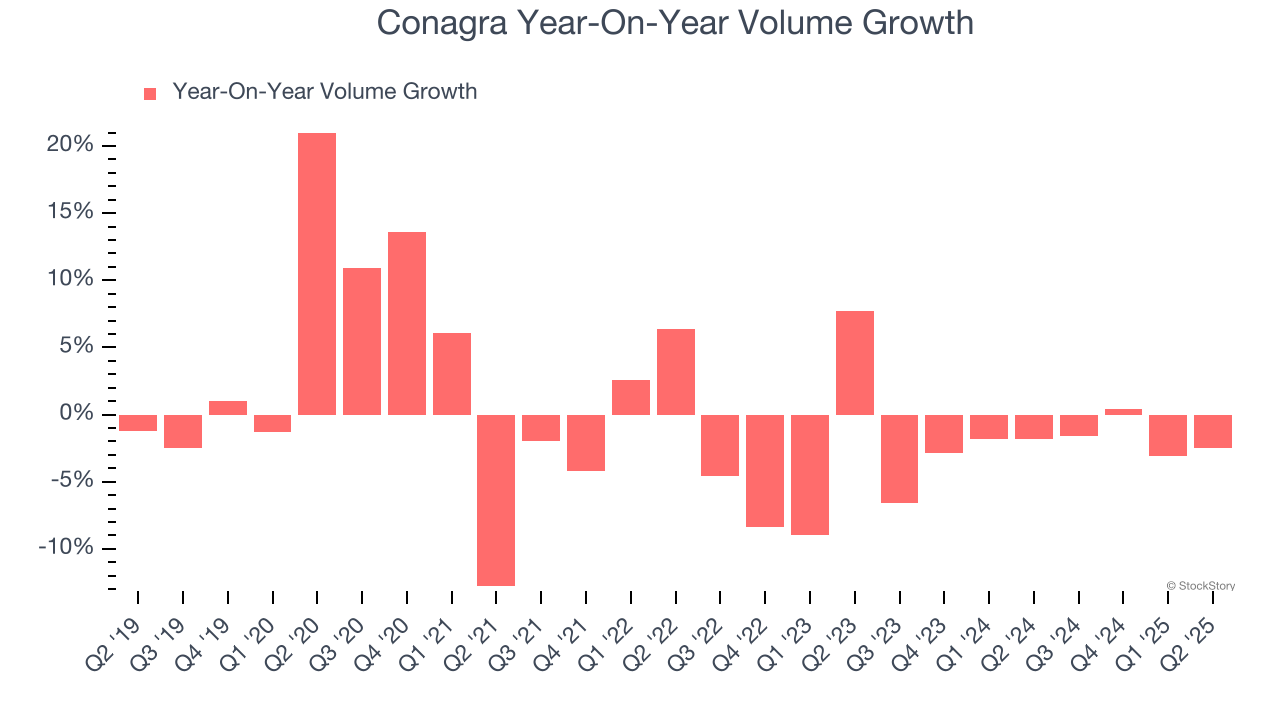

- Sales Volumes fell 2.5% year on year, in line with the same quarter last year

- Market Capitalization: $9.73 billion

Company Overview

Founded in 1919 as Nebraska Consolidated Mills in Omaha, Nebraska, Conagra Brands today (NYSE: CAG) boasts a diverse portfolio of packaged foods brands that includes everything from whipped cream to jarred pickles to frozen meals.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $11.61 billion in revenue over the past 12 months, Conagra is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To expand meaningfully, Conagra likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Conagra struggled to increase demand as its $11.61 billion of sales for the trailing 12 months was close to its revenue three years ago. This is mainly because consumers bought less of its products - we’ll explore what this means in the "Volume Growth" section.

This quarter, Conagra missed Wall Street’s estimates and reported a rather uninspiring 4.3% year-on-year revenue decline, generating $2.78 billion of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 1.6% over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and indicates its products will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Conagra generated its growth (or lack thereof) from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Conagra’s average quarterly volumes have shrunk by 2.5%. This isn’t ideal for a consumer staples company, where demand is typically stable. In the context of its 2.6% average organic sales declines, we can see that most of the company’s losses have come from fewer customers purchasing its products.

In Conagra’s Q2 2025, sales volumes dropped 2.5% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from Conagra’s Q2 Results

We enjoyed seeing Conagra beat analysts’ EBITDA expectations this quarter. On the other hand, its revenue and EPS missed along with its full-year EPS guidance. Overall, this quarter could have been better. The stock traded down 4.2% to $19.50 immediately following the results.

The latest quarter from Conagra’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.