CNO Financial Group has been treading water for the past six months, recording a small loss of 3.4% while holding steady at $36.33. The stock also fell short of the S&P 500’s 7.1% gain during that period.

Is now the time to buy CNO Financial Group, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is CNO Financial Group Not Exciting?

We're sitting this one out for now. Here are three reasons why you should be careful with CNO and a stock we'd rather own.

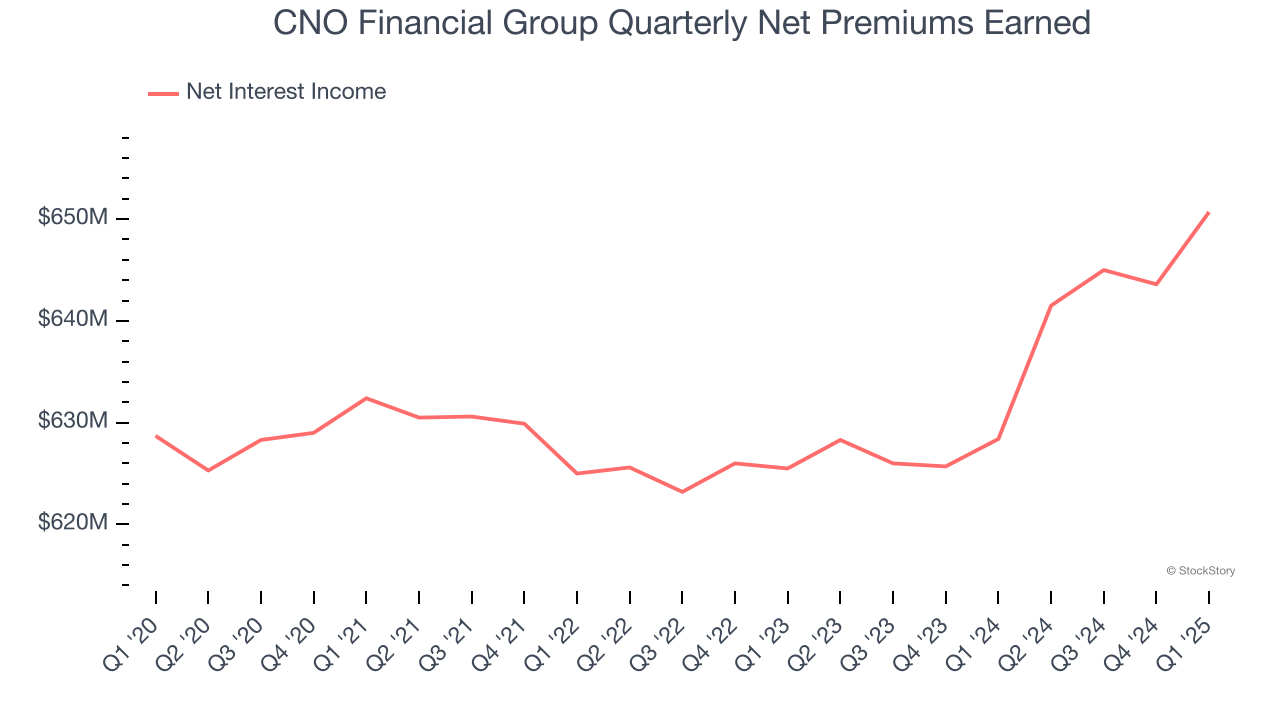

1. Net Premiums Earned Hits a Plateau

While insurers generate revenue from multiple sources, investors view net premiums earned as the cornerstone - its direct link to core operations stands in sharp contrast to the unpredictability of investment returns and fees.

CNO Financial Group’s net premiums earned was flat over the last four years, much worse than the broader insurance industry.

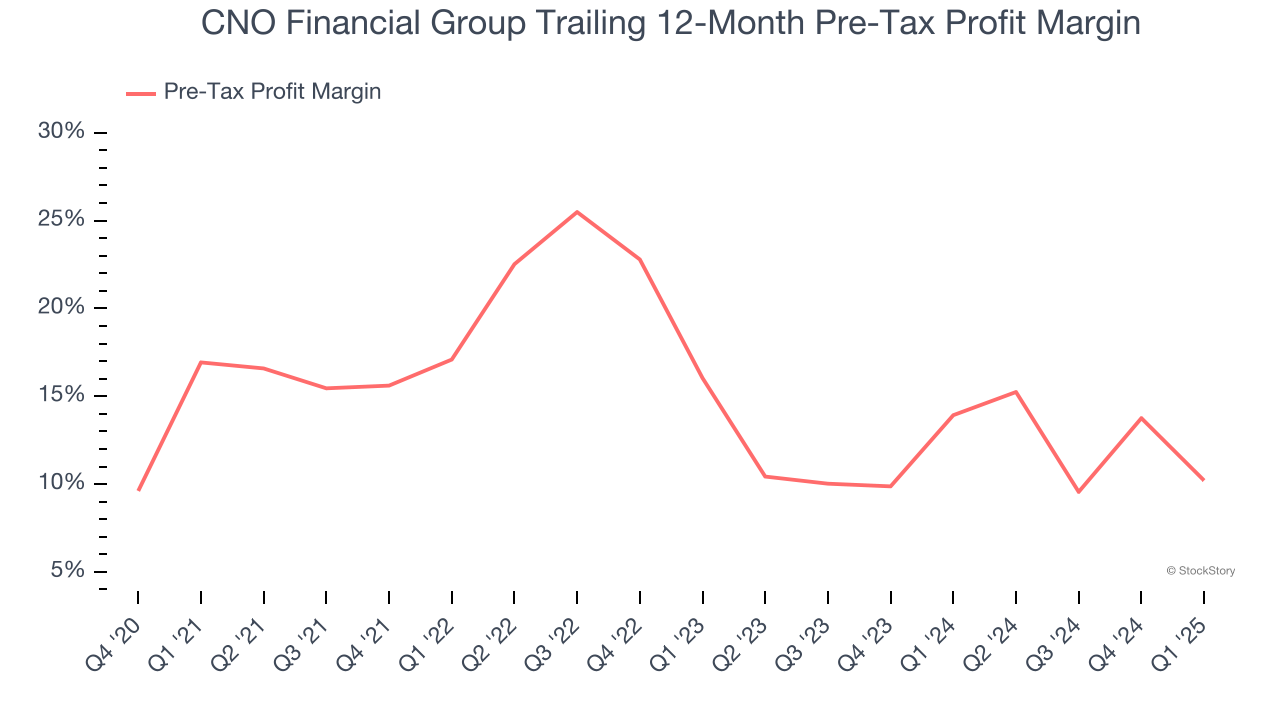

2. Deteriorating Pre-tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because insurers are balance sheet businesses, where assets and liabilities define the core economics. This means that interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last four years, CNO Financial Group’s pre-tax profit margin has fallen by 6.7 percentage points, hitting 10.2% for the past 12 months. Said differently, the company’s expenses have increased at a faster rate than revenue, which is usually raises questions in mature industries (the exception is a high-growth company that reinvests its profits in attractive ventures).

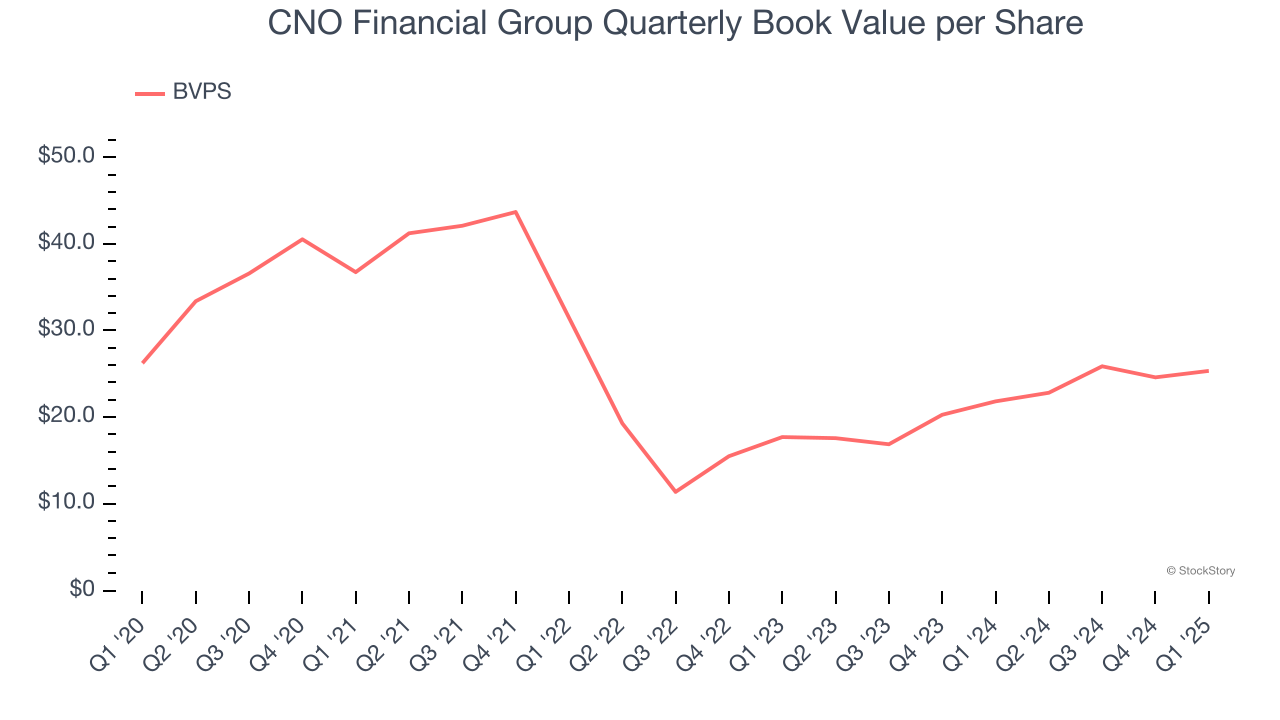

3. Growing BVPS Reflects Strong Asset Base

Book value per share (BVPS) serves as a key indicator of an insurer’s financial stability, reflecting a company’s ability to maintain adequate capital levels and meet its long-term obligations to policyholders.

Although CNO Financial Group’s BVPS was flat over the last five years. the good news is that its growth has recently accelerated as BVPS grew at an impressive 19.7% annual clip over the past two years (from $17.68 to $25.33 per share).

Final Judgment

CNO Financial Group isn’t a terrible business, but it doesn’t pass our quality test. With its shares lagging the market recently, the stock trades at 1.4× forward P/B (or $36.33 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.