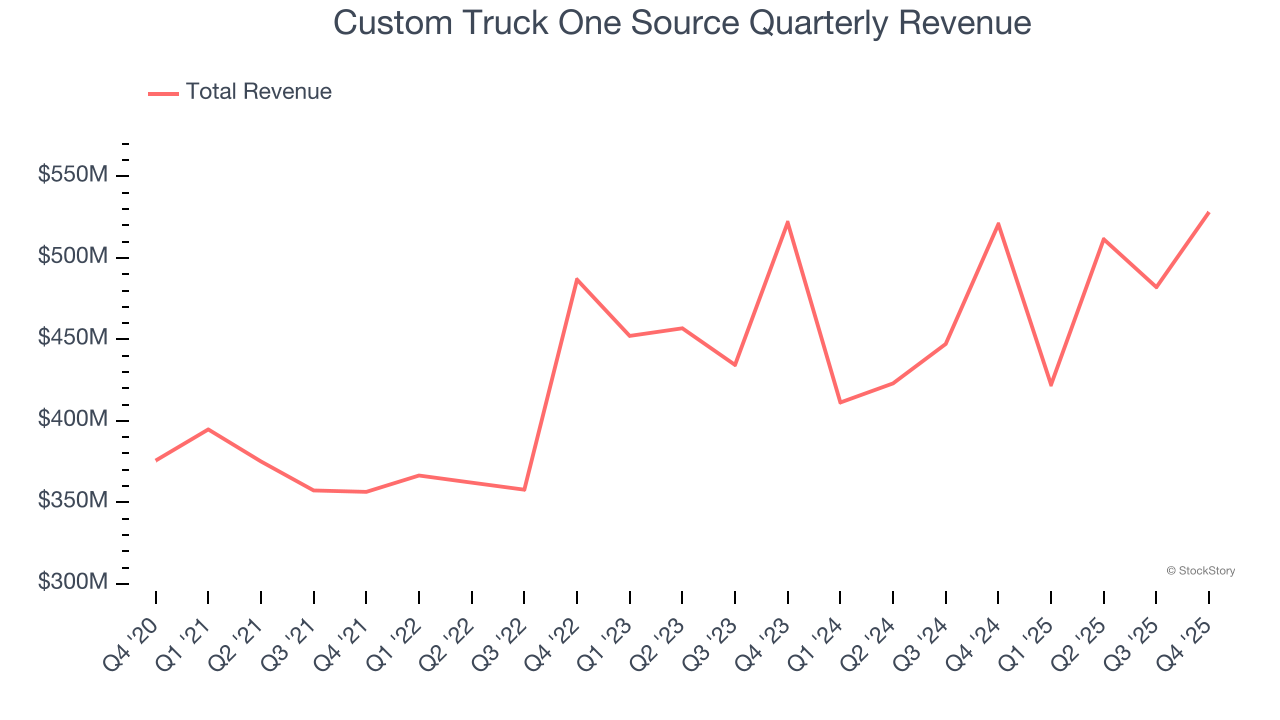

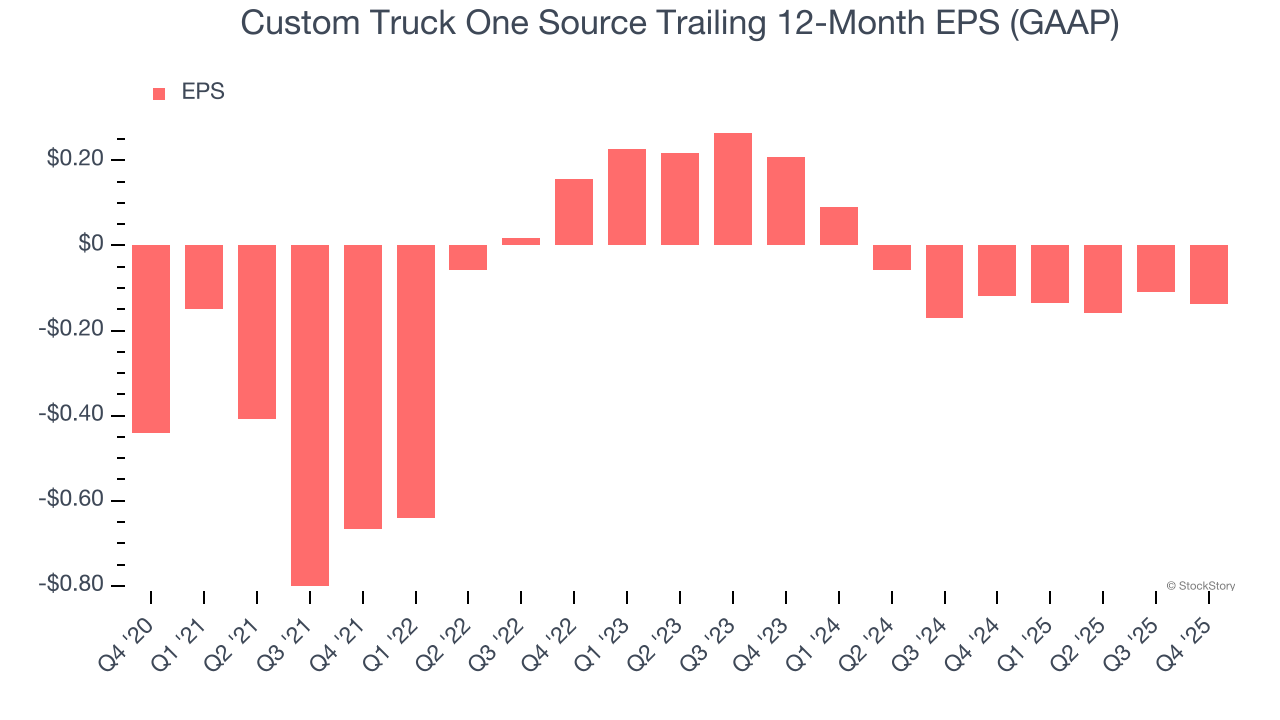

Heavy equipment distributor Custom Truck One Source (NYSE: CTOS) fell short of the market’s revenue expectations in Q4 CY2025 as sales only rose 1.4% year on year to $528.2 million. The company’s full-year revenue guidance of $2.06 billion at the midpoint came in 1.9% below analysts’ estimates. Its GAAP profit of $0.09 per share was 32.9% above analysts’ consensus estimates.

Is now the time to buy Custom Truck One Source? Find out by accessing our full research report, it’s free.

Custom Truck One Source (CTOS) Q4 CY2025 Highlights:

- Revenue: $528.2 million vs analyst estimates of $581 million (1.4% year-on-year growth, 9.1% miss)

- EPS (GAAP): $0.09 vs analyst estimates of $0.07 (32.9% beat)

- Adjusted EBITDA: $120.7 million vs analyst estimates of $115.8 million (22.9% margin, 4.2% beat)

- EBITDA guidance for the upcoming financial year 2026 is $422.5 million at the midpoint, in line with analyst expectations

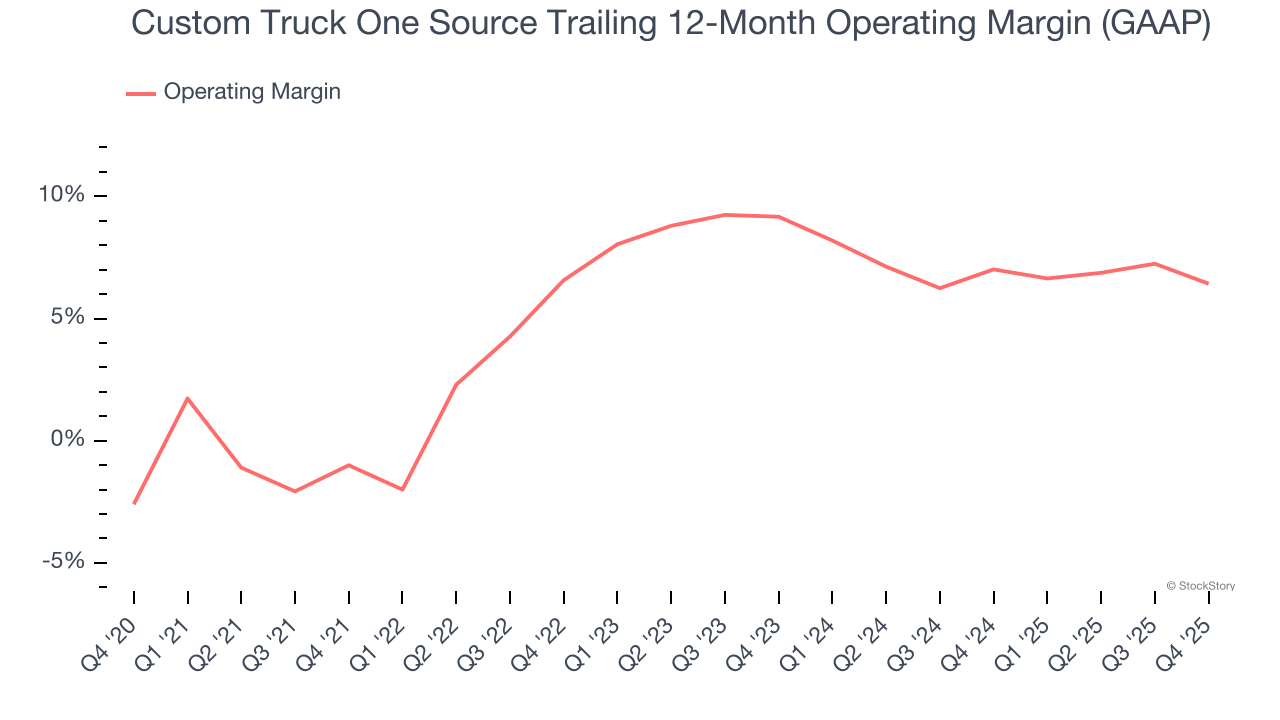

- Operating Margin: 9.8%, down from 12.9% in the same quarter last year

- Free Cash Flow was -$60.75 million compared to -$37.76 million in the same quarter last year

- Backlog: $335.3 million at quarter end, down 9.1% year on year

- Market Capitalization: $1.45 billion

“In the fourth quarter, we achieved record quarterly revenue, as well as sequential and year-over-year improvement in both revenue and Adjusted EBITDA, delivering 18% Adjusted EBITDA growth in the quarter and 13% for the full year. The significant improvements in our core T&D markets that we experienced in the third quarter continued into the fourth quarter, positioning our ERS segment to finish the year with 20% revenue growth in the fourth quarter and 17% for the full year. For the quarter, our rental fleet achieved average utilization of almost 84%, the highest levels in nearly three years. We ended the year with total OEC of $1.64 billion, the highest in our history, which should support our expected growth within ERS in 2026,” said Ryan McMonagle, Chief Executive Officer of CTOS.

Company Overview

Inspired by a family gas station, Custom Truck One Source (NYSE: CTOS) is a distributor of trucks and heavy equipment.

Revenue Growth

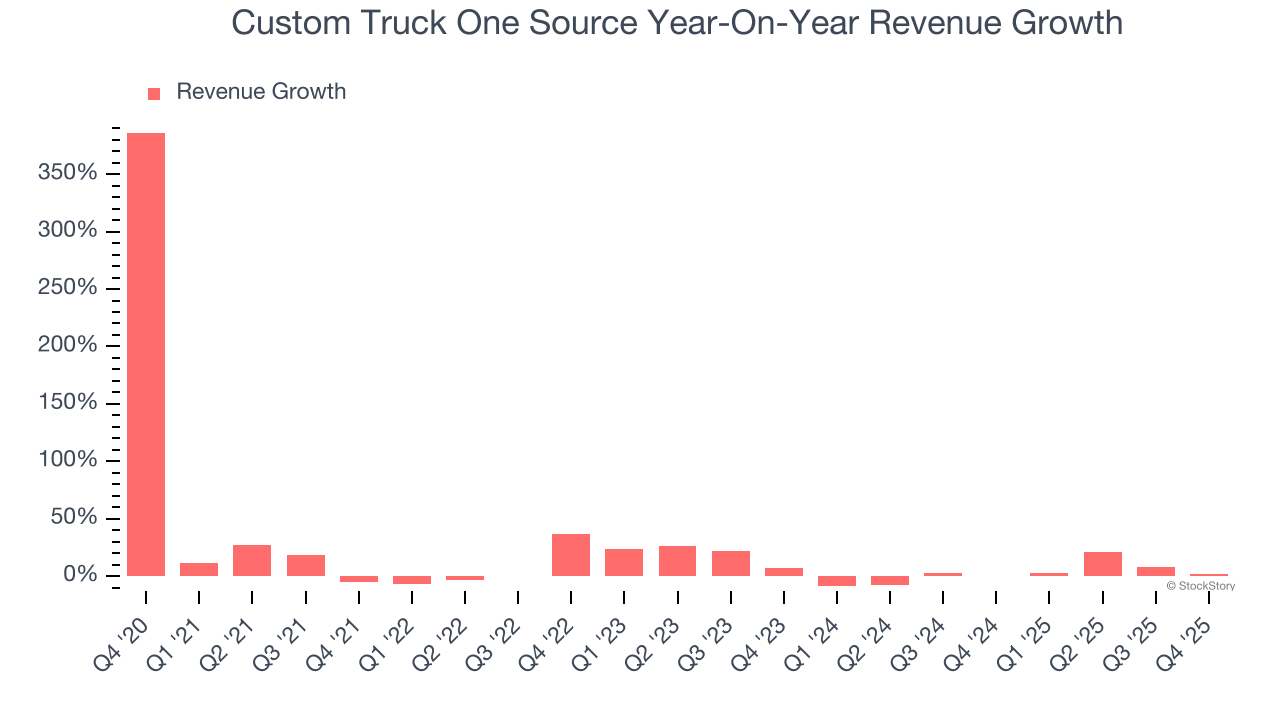

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Custom Truck One Source’s 7.9% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Custom Truck One Source’s recent performance shows its demand has slowed as its annualized revenue growth of 2.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Custom Truck One Source also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Custom Truck One Source’s backlog reached $335.3 million in the latest quarter and averaged 9.1% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Custom Truck One Source’s revenue grew by 1.4% year on year to $528.2 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.5% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Custom Truck One Source was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.9% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Custom Truck One Source’s operating margin rose by 7.4 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Custom Truck One Source generated an operating margin profit margin of 9.8%, down 3.1 percentage points year on year. Since Custom Truck One Source’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Custom Truck One Source’s full-year earnings are still negative, it reduced its losses and improved its EPS by 20.6% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Custom Truck One Source, its EPS declined by 63.4% annually over the last two years while its revenue grew by 2.1%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Custom Truck One Source reported EPS of $0.09, down from $0.12 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Custom Truck One Source’s full-year EPS of negative $0.14 will flip to positive $0.03.

Key Takeaways from Custom Truck One Source’s Q4 Results

It was good to see Custom Truck One Source beat analysts’ EPS expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $6.38 immediately following the results.

Is Custom Truck One Source an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).