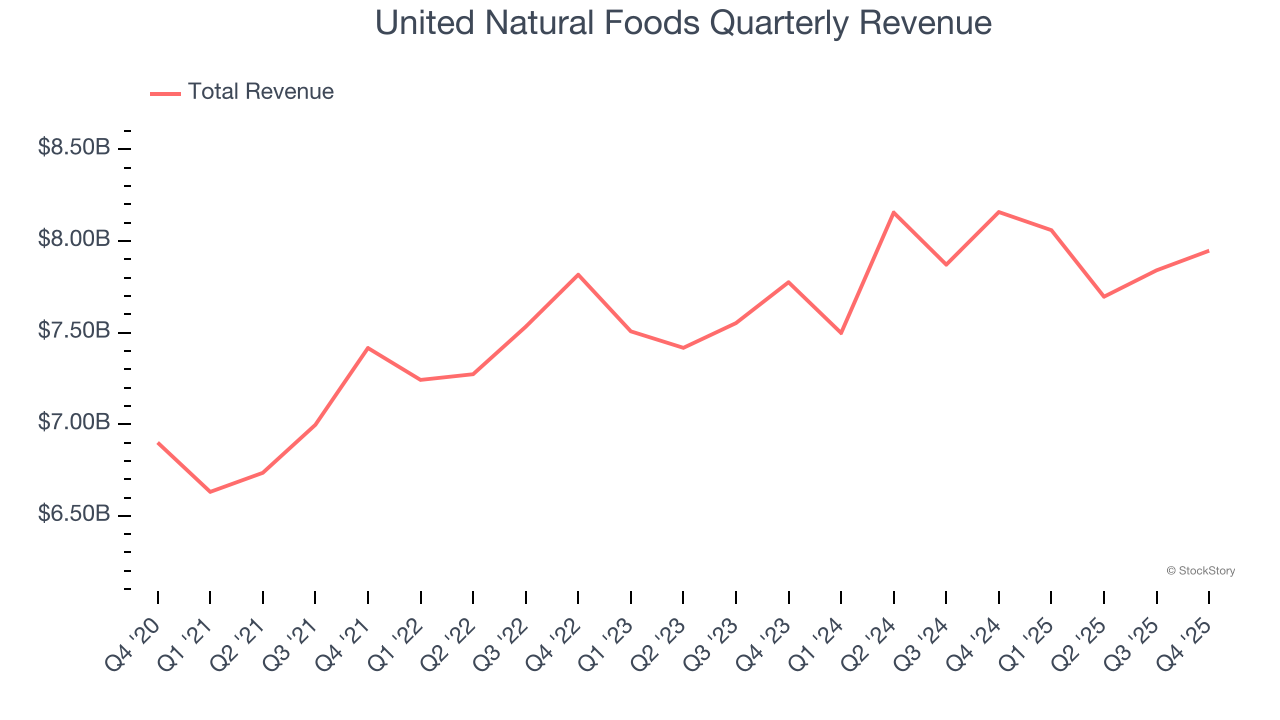

Food distribution company United Natural Foods (NYSE: UNFI) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 2.6% year on year to $7.95 billion. The company’s full-year revenue guidance of $31.2 billion at the midpoint came in 2.3% below analysts’ estimates. Its non-GAAP profit of $0.62 per share was 22.7% above analysts’ consensus estimates.

Is now the time to buy United Natural Foods? Find out by accessing our full research report, it’s free.

United Natural Foods (UNFI) Q4 CY2025 Highlights:

- Revenue: $7.95 billion vs analyst estimates of $8.11 billion (2.6% year-on-year decline, 2% miss)

- Adjusted EPS: $0.62 vs analyst estimates of $0.51 (22.7% beat)

- Adjusted EBITDA: $179 million vs analyst estimates of $167.2 million (2.3% margin, 7% beat)

- The company dropped its revenue guidance for the full year to $31.2 billion at the midpoint from $31.8 billion, a 1.9% decrease

- EBITDA guidance for the full year is $695 million at the midpoint, above analyst estimates of $674.6 million

- Operating Margin: 0.7%, in line with the same quarter last year

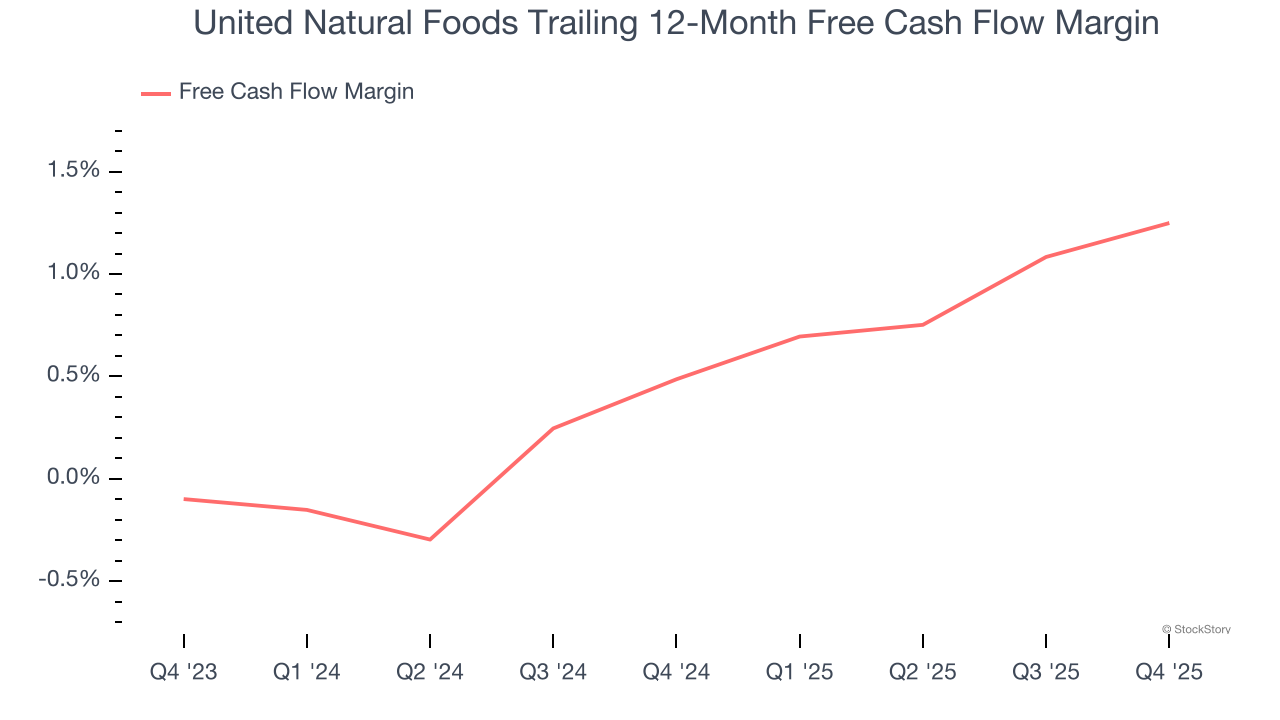

- Free Cash Flow Margin: 3.1%, similar to the same quarter last year

- Market Capitalization: $2.37 billion

Company Overview

With a vast network of 55 distribution centers spanning approximately 30 million square feet of warehouse space, United Natural Foods (NYSE: UNFI) is North America's premier grocery wholesaler distributing natural, organic, and conventional products to over 30,000 retail locations across the US and Canada.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $31.54 billion in revenue over the past 12 months, United Natural Foods is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To expand meaningfully, United Natural Foods likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, United Natural Foods grew its sales at a sluggish 1.8% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, United Natural Foods missed Wall Street’s estimates and reported a rather uninspiring 2.6% year-on-year revenue decline, generating $7.95 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months, similar to its three-year rate. This projection is underwhelming and indicates its newer products will not accelerate its top-line performance yet.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

United Natural Foods broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

United Natural Foods’s free cash flow clocked in at $243 million in Q4, equivalent to a 3.1% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

Key Takeaways from United Natural Foods’s Q4 Results

We enjoyed seeing United Natural Foods beat analysts’ EBITDA and EPS expectations this quarter. On the other hand, its full-year revenue guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this print could have been better. Investors were likely hoping for more, and shares traded down 1.5% to $38.49 immediately following the results.

Big picture, is United Natural Foods a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).