Costco (COST) is among the leading retailers investors pay the closest attention to right now. There's good reason for this. With one of the biggest footprints in North America and a membership model that provides excellent free cash flow growth, this is a retailer with one of the most unique moats around its underlying business that's led to incredible stock price appreciation over time.

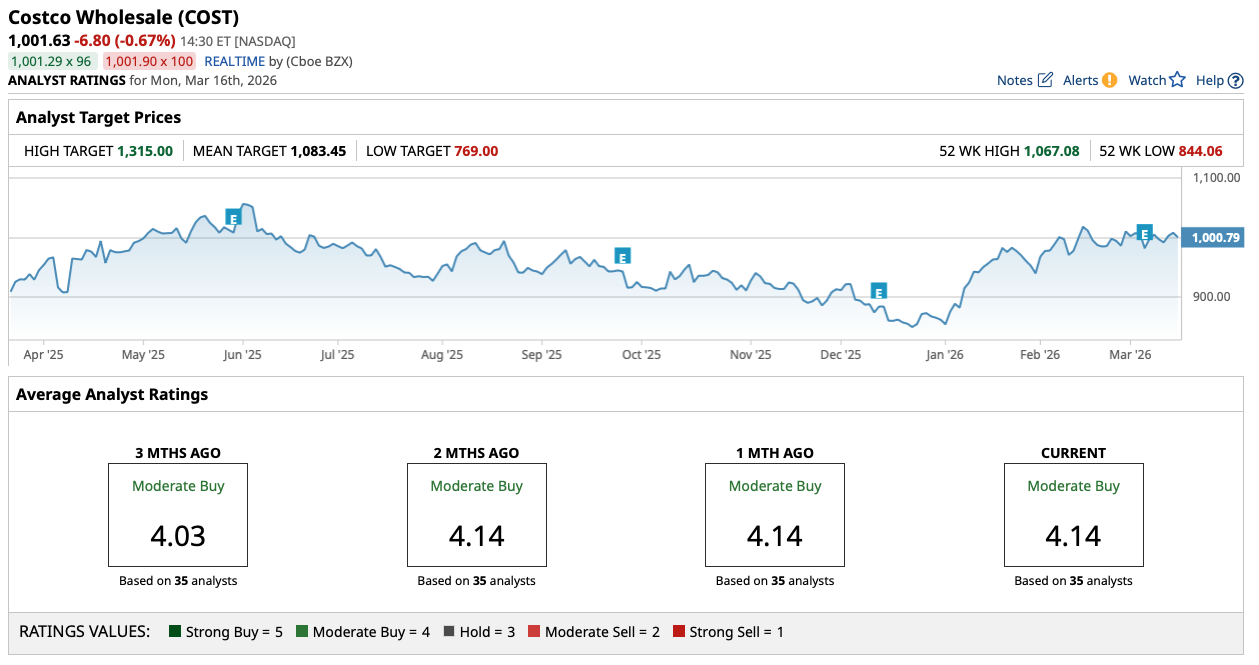

As the chart above shows, it's been a rocky few months for this top-tier blue-chip retail stock. Dipping to a low around $850 per share late last year and into the beginning of 2026, COST stock has since rebounded toward the $1000 level (currently trading just above this key psychological threshold). As such, it's clear many investors are starting to pay attention to the bullish narrative around Costco, which includes key factors such as digital growth, customer loyalty, and future growth strategies the company's management team is implementing.

Let's dive into what to make of this bullish assessment of COST and whether this retail stock can continue to climb into the end of this year (and for years to come).

What's Driven Costco's Recent Decline, and What Could Go Right?

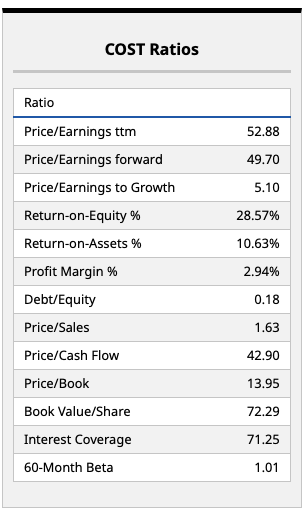

I think it's important to start this discussion around the bull case for Costco's stock with commentary around what's ailing the company. I think most of the recent downturn in COST stock has to do with the ultra-premium multiple the market has granted Costco.

Trading at nearly 50 times forward earnings, Costco is certainly among the most expensive growth stocks in the market right now. Indeed, for a retailer, this multiple is one that's almost unheard of.

Again, it's Costco's premium membership model, its value, quality, and fresh merchandise, and a customer base that's among the most loyal in the shopping world that are driving this multiple. Member numbers have been very consistent and resilient, with many market participants seemingly happy to pay this multiple with the knowledge that there's some recession-resistant upside over the long term.

Now, past earnings results did show strong performance on all lines, with the company's fuel business continuing to shine bright. Given the surge in gasoline prices we're seeing of late, Costco's below-market pricing for its gas stations at most locations provides an apparent thesis for investors to grasp onto. More consumers seeking discounts on gas will continue to flock to Costco and drive foot traffic volume within its stores. It's that consistent and stable loss-leader strategy that has so many consumers coming back for more, and it's one key reason I'm personally a member.

With plenty of room for optimization and efficiency improvements, particularly in the world of digital and international business operations, there's a lot to like about how Costco is positioned here. So long as investors believe that the current market multiple for COST stock aligns with its long-term growth prospects, this is a stock that could have material upside over the long term.

Just How Much Long-Term Upside Are Analysts Pricing In?

The good news for Costco bulls is that Wall Street analysts appear to be just as bullish on this top-tier retailer as Main Street. A consensus price target of $1,083.45 per share prices in around 8% upside from current levels and suggests to me that this recent rally is one that should have been expected.

Indeed, at around $850 per share to start this year, I'd argue that COST stock provided incredible value to investors at that time. Still, 8% upside potential is nothing to sneeze at, and I actually think that target could end up being light, particularly if Costco has another few quarters of significant earnings beats ahead.

On the other side of the coin, it's also true that valuation multiples for many top names appear to be under pressure. As such, there could be heightened downside risk with this name. That's the game investors are playing, and that's what makes markets. But overall, I'm remaining bullish on Costco over the long term and will look for entry points to get in around the $850 level moving forward.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart