Investors may be hesitant to put fresh money into stocks now as market volatility surges. The CBOE Volatility Index is one of the most widely used indicators to measure market risk and investor sentiment. Recently, it climbed above 20 and briefly spiked near 28, its highest level of 2026 so far, driven in part by ongoing conflict in the Middle East.

During such uncertain periods, investors prefer safer assets over growth stocks. However, not every growth opportunity should be overlooked. While software stocks are struggling now, Braze (BRZE) could be an excellent buy-and-hold opportunity over the next several years.

3 Reasons to Buy Braze Stock Now

Braze is a cloud-based SaaS (software-as-a-service) company that provides a customer engagement platform. It helps businesses send personalized messages to customers across channels like mobile push notifications, email, in-app messaging, and web notifications, using real-time customer data and analytics.

BRZE stock is down 41% year-to-date (YTD), but analysts predict triple-digit upside in 2026.

Even though many software stocks are struggling right now due to AI disruption fears and falling valuations, high-quality platforms with strong customer engagement capabilities like Braze may emerge as long-term winners. Here are three reasons that support the bull case for Braze:

1. Strong Growth Despite a Tough Software Market

Braze is still growing rapidly even when many SaaS companies are slowing down. In the third quarter of fiscal 2026, the company reported $191 million in revenue, an increase of 25.5% year-over-year (YoY). The company is also adding customers at a rapid pace. Total customers reached 2,528, up 14% YoY, while the number of large customers spending at least $500,000 annually increased 29% to 303 accounts.

Furthermore, remaining performance obligations (or RPO) stood at $891.4 million in Q3, out of which management expects to recognize $572.7 million in less than a year. This shows that demand for Braze’s customer engagement platform across industries and geographies remains strong.

2. Profitability Is Improving

Beyond revenue growth, Braze is also improving its profitability. The company has now reported four consecutive quarters of adjusted operating income and six straight quarters of adjusted net income. Braze also generated $18 million in free cash flow in Q3. The company expects to report a profit in Q4, with full-year adjusted earnings in the range of $0.42 to $0.43 per share, up from $0.17 per share in fiscal 2025. This shift toward profitability reduces risk associated with most high-growth tech stocks.

3. AI Is Driving Product Adoption

Braze is investing extensively in AI-powered customer engagement, which might provide a significant competitive advantage. Its AI tools help businesses personalize marketing campaigns, automate customer engagement decisions, and generate content more efficiently. Management emphasized that a large e-commerce customer using Braze’s AI decisioning tools saw a 12% increase in app downloads and a 15% rise in premium membership conversions.

Analysts expect Braze's revenue to increase by 23.2% to $731.2 million in fiscal 2026, while earnings are projected to increase by 147.6%. In fiscal 2027, earnings could rise another 51.3% to $0.64 per share on $858.4 million in revenue. Currently, the stock trades at roughly 30× forward 2027 earnings. While investors have been concerned that many software stocks are overvalued and unable to justify their premium valuations, Braze’s P/E multiple appears reasonable given its strong double-digit revenue growth and rapid earnings expansion over the next two years.

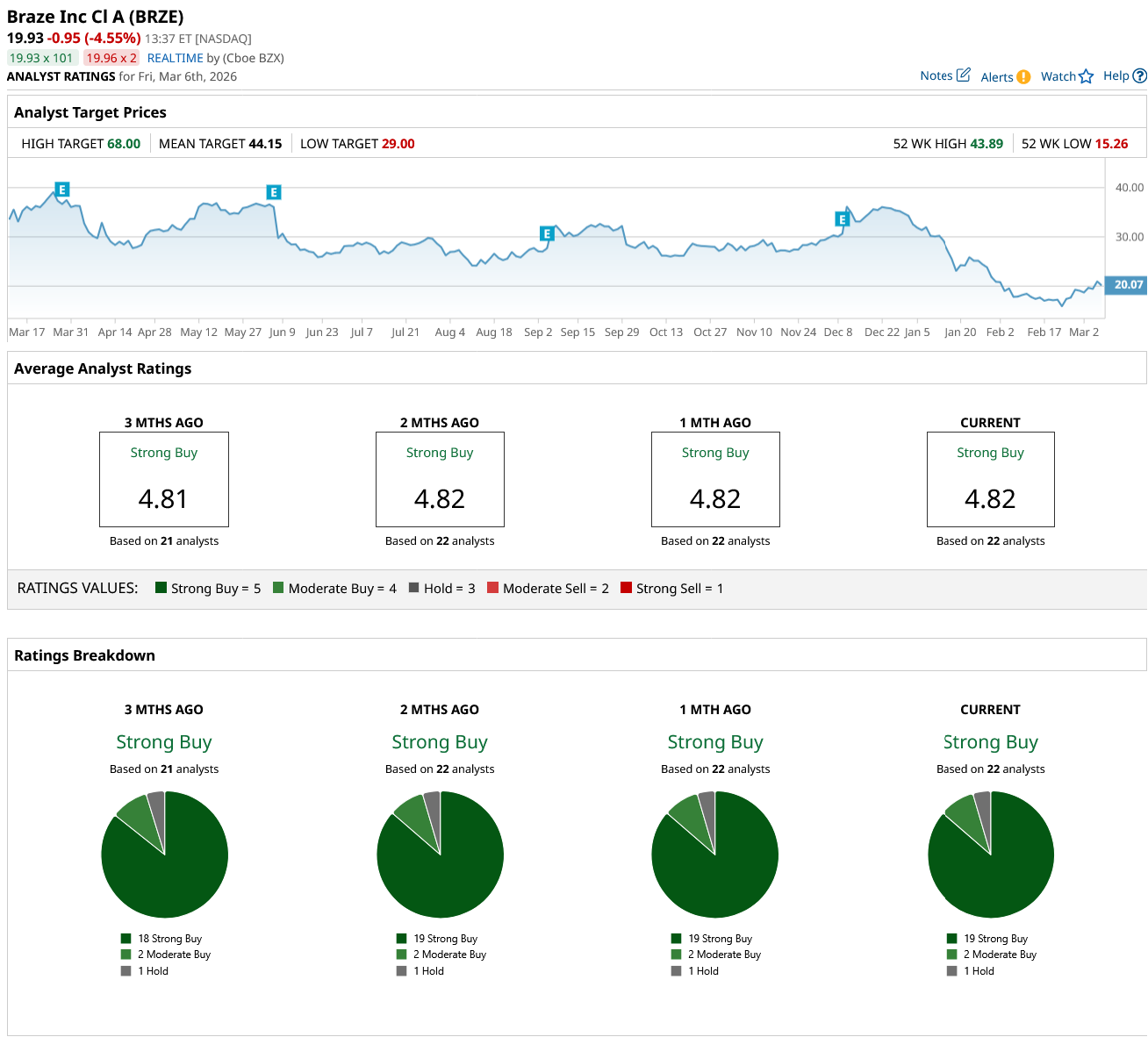

What Is the Target Price for BRZE Stock?

Overall, Wall Street rates BRZE stock a “Strong Buy.” Of the 22 analysts covering Braze's stock, 19 rate it a “Strong Buy,” while two recommend a “Moderate Buy,” and one recommends a “Hold.”

Analysts have given a mean target price of $44.15 to BRZE stock, which implies an upside potential of 122% from current levels. Plus, its high target price of $68 suggests that the stock could rise as high as 241% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Marvell Breaks Through Key Resistance Levels, Should You Chase the Rally in MRVL Stock?

- Apple Just Unveiled the New iPhone 17e. Should You Buy, Sell, or Hold AAPL Stock Now?

- College Decision Day Is Just Around the Corner. Warren Buffett Says ‘I Never Look at Where a Candidate Has Gone to School. Never!’

- Will the Iran War Trigger a 2025-Like Rally in Netflix Stock?