Peraso (PRSO) shares more than doubled on Friday after the San Jose-headquartered firm said it has secured a sizable defense contract from InTACT. The defense contractor has picked PRSO’s 60 GHz mmWave technology for next-generation drone Identification Friend or Foe (IFF) systems, it revealed in a press release dated March 6.

Despite this meteoric run, Peraso stock remains down more than 30% versus its 52-week high.

Does InTACT News Warrant Buying Peraso Stock?

The InTACT partnership is a major strategic milestone, as it validates PRSO’s millimeter-wave tech for high-stakes military applications.

In the context of the escalating U.S.-Iran war, the demand for sophisticated drone tech has reached a fever pitch — and Peraso’s 60 GHz beamforming chips allow for “highly directional, low-power” communication that’s nearly impossible for adversaries to jam or intercept. This stealth communication is vital for IFF systems, preventing friendly fire in cluttered warzones.

For investors, this contract signals PRSO stock is pivoting from a pure-play 5G component maker to a critical defense subcontractors, opening the door to massive Department of Defense spending cycles and multi-year procurement deals.

PRSO Shares Remain Super Risky to Own

Despite InTACT news, the fundamental bear case for Peraso remains daunting given it’s still a penny stock, making it prone to extreme volatility and pump-and-dump schemes. And even financially, the picture isn’t any rosier. PRSO continues to lose money, posting a negative 39% profit margin with less than a year of cash runway.

Additionally, the company more than doubled its float in 2025, massively diluting its existing shareholders just to remain listed.

Still, Peraso shares were trading at less than $1 before winning the InTACT defense contract, which means the risk of a reverse split or further dilution remains on the table.

How Wall Street Recommends Playing Peraso

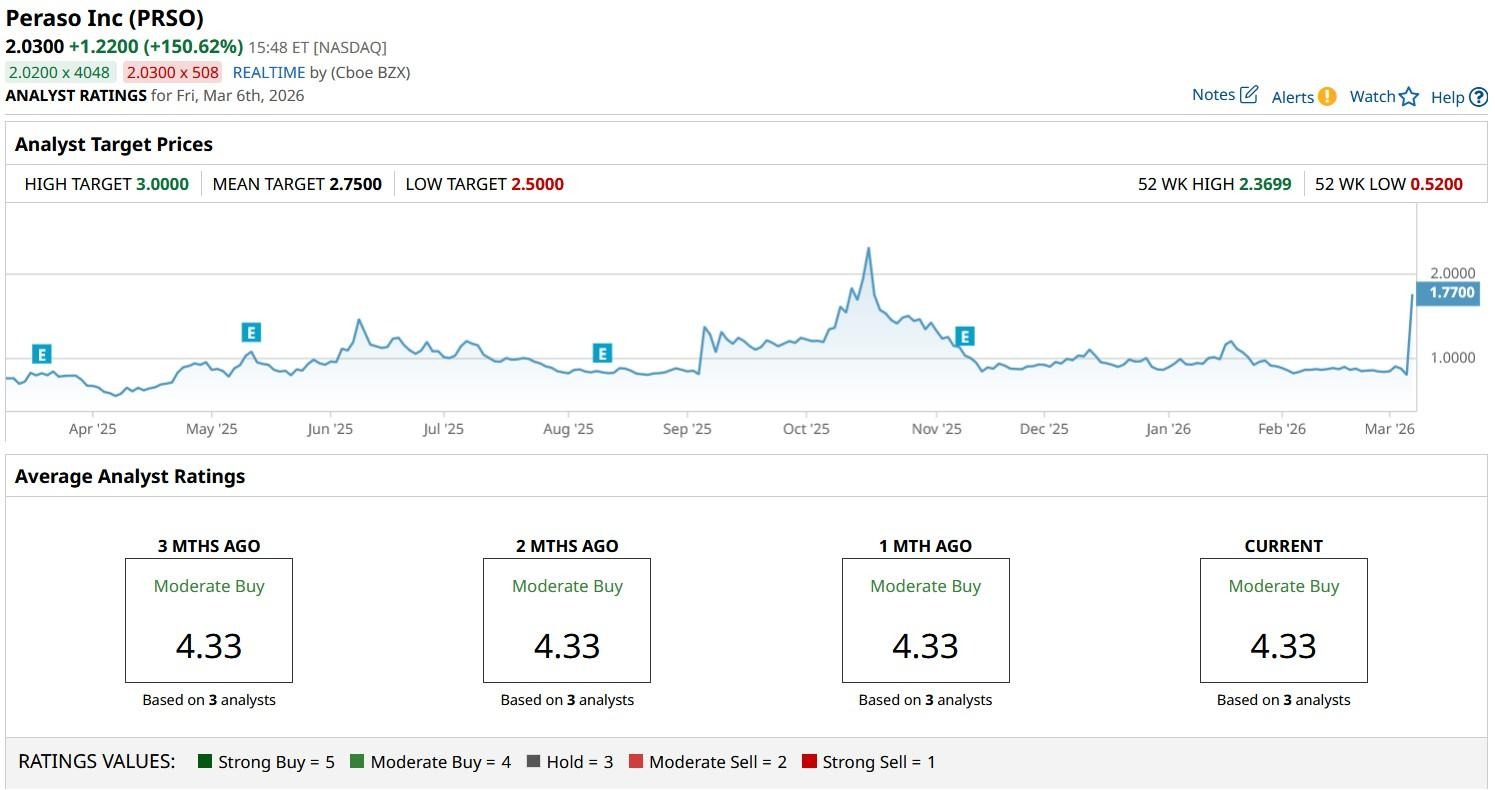

PRSO shares’ relative strength index (14-day) now sits in early 80s, indicating deeply overbought conditions. Still, Wall Street sees them as undervalued at current levels.

According to Barchart, the consensus rating on Peraso sits at “Moderate Buy” currently, with the mean target of $2.75 indicating potential upside of more than 60% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Penny Stock Is Soaring on a New Drone Contract Win. Should You Buy Peraso Here Amid U.S.-Iran War?

- A $100 Billion and More Reasons to Buy Broadcom Stock Now

- As Marvell Breaks Through Key Resistance Levels, Should You Chase the Rally in MRVL Stock?

- Apple Just Unveiled the New iPhone 17e. Should You Buy, Sell, or Hold AAPL Stock Now?