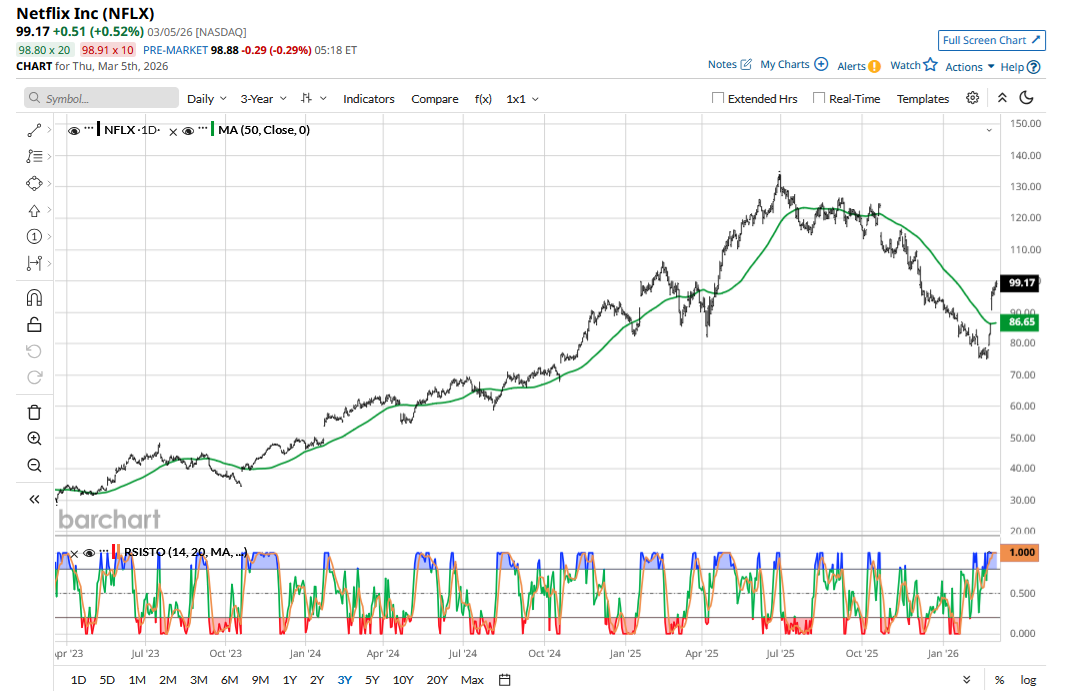

While the broader markets have been under pressure and tech stocks have particularly fallen hard this year, Netflix is up almost 20% over the last month. In my previous article, I had noted that NFLX’s risk-reward was looking attractive. With the stock up sharply from those levels, let’s explore whether the streaming giant is still a worthy investment.

Why Is Netflix Stock Going Up?

Much of Netflix’s recent gains could be attributable to the company walking away from acquiring Warner Bros. (WBD) assets. Markets had sent a loud and clear message, and the stock had been slumping ever since Netflix announced the transaction in December 2025. NFLX stock soared after the company gave up on what would have been its largest-ever acquisition, ending the bidding war with Paramount Skydance (PSKY). Netflix didn’t exactly walk out empty-handed, though, and would get $2.8 billion as a breakup fee.

Along with the immediate trigger of the WBD deal, the macro environment is also conducive to the rally in Netflix, which is a defensive play. To begin with, fears of an artificial intelligence (AI) bubble and the selloff in software stocks have made some investors wary of tech stocks. Secondly, after a brief lull, trade uncertainty is back on the table with President Donald Trump announcing fresh sweeping tariffs after his previous ones were nixed by the Supreme Court. However, the new tariffs would also face legal scrutiny, with two dozen states suing Trump over them.

To make things worse, Judge Richard Eaton of the U.S. Court of International Trade in Manhattan ordered the government to refund the previously collected tariffs, which could deteriorate the already precarious fiscal math.

The Iran war is further adding to the gloom, as higher energy prices would have been the last thing that central banks and governments globally would have wanted. Benign energy prices helped tame inflation and provided breathing space to central bankers, including Powell and Co. in the U.S., to cut interest rates. With inflation already looking sticky and stubbornly above the Fed’s 2% mandate, higher energy prices further lower the probability of rate cuts this year, even if Trump nominee Kevin Warsh takes over the baton from Powell this year.

Netflix Is a Defensive Play

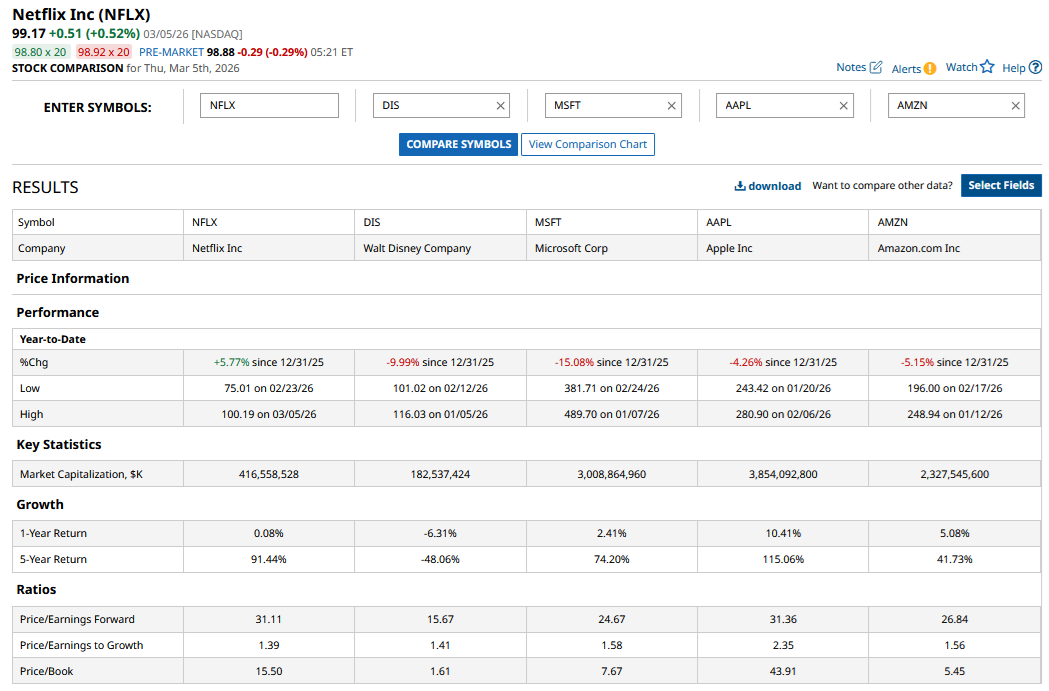

Among tech names, Apple (AAPL) and Microsoft (MSFT) were seen as prominent defensive plays given their rock-solid balance sheets and stable businesses. However, while Apple’s rich valuations limit its upside, Microsoft has somewhat lost its defensive status as it continues to plow billions into AI.

Netflix, meanwhile, has emerged as a defensive play, which was on full display in 2025 when it outperformed big time in the first half of the year amid trade war fears. For most users, their Netflix subscriptions won’t be the first discretionary spending or subscriptions to be axed in difficult economic times.

A Netflix subscription has become an almost utility-like service for most subscribers, including me. The company capitalized on the moat in its business by cracking down on password sharing, cajoling many customers who were watching its content through shared passwords to buy their own subscription.

The ad-supported tier was another success story and helped Netflix add millions of subscribers. The company’s ad business continues to grow well, and revenues rose over 2.5x to $1.5 billion last year. The company expects revenues to “roughly double” this year as it capitalizes on a growing subscription base on the ad-supported tier.

Should You Buy NFLX Stock?

Given “SaaS-pocalypse” fears, I would be wary of classifying Netflix as a “software” company, but the company’s business model is not very different from that of a software company. The streaming industry has high operating leverage, as the content and technology costs are largely fixed. The cost to create new content is also agnostic of subscriber base, even as a rising global subscriber base would warrant higher content spending to retain members and attract new ones.

The company’s operating margins hit almost 30% last year, and it expects them to keep rising as revenue growth outstrips content expense, resulting in margin expansion.

Netflix’s valuation multiples have expanded amid the recent rally, and it trades at a forward price-to-earnings (P/E) multiple of just over 31x. While the margin of safety is somewhat lower than it was prior to the surge, I am constructive on the stock at these levels and see it as a tactical buy amid the broader market weakness.

NFLX outperformed markets hands down in the first half of 2025, and I won’t be surprised to see similar results this year if the Iran war escalates. Even if things stabilize in the Middle East, the stock could still deliver decent returns over the next couple of years, given the reasonable valuations and strong growth outlook.

On the date of publication, Mohit Oberoi had a position in: NFLX , MSFT , AAPL . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A $100 Billion and More Reasons to Buy Broadcom Stock Now

- As Marvell Breaks Through Key Resistance Levels, Should You Chase the Rally in MRVL Stock?

- Apple Just Unveiled the New iPhone 17e. Should You Buy, Sell, or Hold AAPL Stock Now?

- College Decision Day Is Just Around the Corner. Warren Buffett Says ‘I Never Look at Where a Candidate Has Gone to School. Never!’