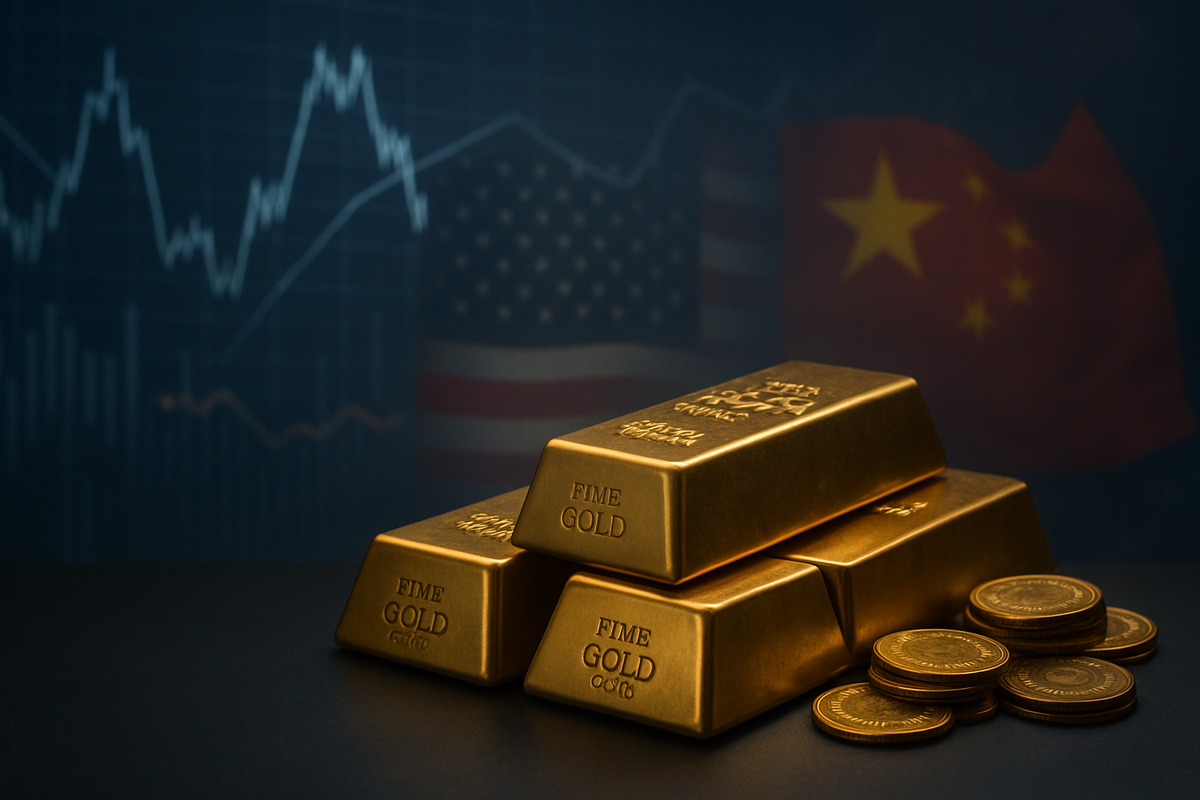

New York, NY – October 16, 2025 – Gold prices on the Comex futures exchange have shattered previous records today, surging to an unprecedented $4,288 per ounce. This historic rally is primarily fueled by a dramatic escalation in trade tensions between the United States and China, prompting a widespread flight to safe-haven assets among investors grappling with heightened global uncertainty. The immediate aftermath has seen a significant shift towards risk-off sentiment across financial markets, with analysts now recalibrating their price targets for the precious metal, many forecasting further gains.

The record-breaking ascent of gold underscores the profound impact of geopolitical instability on financial markets. As the world's two largest economies engage in a renewed and intensifying trade confrontation, investors are increasingly seeking the perceived security of gold. This surge marks a significant milestone in gold's sustained rally throughout 2025, reflecting a year of robust institutional demand, central bank accumulation, and substantial inflows into exchange-traded funds, all indicative of a market bracing for prolonged uncertainty.

Escalating Trade War Propels Gold to Uncharted Territory

The immediate catalyst for gold's spectacular rise to $4,288 per ounce on Comex today is the rapidly deteriorating relationship between the United States and China. What began as intermittent trade disputes has snowballed into a major economic and diplomatic confrontation, with both nations implementing and threatening severe retaliatory measures. This intensification has created a palpable sense of unease across global markets, driving investors en masse to traditional safe havens.

Key developments leading to this critical juncture include a stark warning from US President Donald Trump, threatening to impose 100% tariffs on a broad range of Chinese imports, effective November 1st. This aggressive stance is reportedly in response to perceived breaches of existing trade agreements and China's strategic actions concerning critical resources. Concurrently, the US has tightened restrictions on China's access to vital software technologies, further constricting Beijing's technological advancement capabilities. China has not remained passive, retaliating by curbing its export of rare earth minerals, which are indispensable for numerous high-tech and manufacturing industries globally. Both nations have also initiated special port charges on each other's vessels, and China has sanctioned five US units of a South Korean shipbuilder, alongside halting US soybean purchases – a move that has prompted threats of a cooking oil embargo from President Trump. The diplomatic front also shows severe strain, with President Trump expressing disinterest in a previously scheduled meeting with Chinese President Xi Jinping, signaling a breakdown in high-level dialogue aimed at de-escalation.

Beyond the immediate trade hostilities, several other factors are contributing to gold's heightened appeal. Expectations of further monetary easing by the US Federal Reserve are firm, with markets pricing in a high probability of multiple interest rate cuts before year-end, which typically devalues the dollar and makes gold more attractive. The ongoing US government shutdown adds another layer of domestic uncertainty, while broader geopolitical tensions, including the lingering Russia-Ukraine war, continue to bolster gold's enduring status as a primary safe-haven asset. The confluence of these global and domestic pressures has created a perfect storm, propelling gold to its current record valuation.

Market Winners and Losers in the Golden Rush

The unprecedented surge in gold prices to $4,288 per ounce on Comex is creating a clear divide between potential winners and losers in the financial markets, profoundly impacting various public companies and sectors. For gold mining companies, this environment presents a significant boon. Firms like Barrick Gold Corp. (NYSE: GOLD), Newmont Corporation (NYSE: NEM), and Agnico Eagle Mines Limited (NYSE: AEM) are poised to see substantial increases in their revenues and profitability. Higher gold prices directly translate to fatter margins, assuming production costs remain relatively stable. These companies may also experience a surge in investor interest, potentially driving up their stock valuations and providing capital for exploration and expansion. Furthermore, companies involved in gold streaming and royalty, such as Franco-Nevada Corporation (NYSE: FNV), will also benefit from the increased value of the gold they are entitled to receive.

Conversely, sectors sensitive to economic uncertainty and higher commodity prices face headwinds. Manufacturing companies heavily reliant on rare earth minerals, such as Tesla Inc. (NASDAQ: TSLA) or Apple Inc. (NASDAQ: AAPL), could suffer from China's export curbs, leading to supply chain disruptions and increased input costs. Similarly, industries dependent on international trade, particularly those with significant exposure to US-China commerce, like Boeing Co. (NYSE: BA) or General Motors Co. (NYSE: GM), will likely experience reduced demand and increased operational complexities due to tariffs and trade restrictions. Financial institutions with substantial exposure to emerging markets or riskier assets may also face challenges as investors pull back from these areas in favor of safer havens. Companies involved in the agriculture sector, particularly those exporting to China like Archer-Daniels-Midland Company (NYSE: ADM), could see revenues impacted by China's halt on US soybean purchases and potential further embargoes. The overall risk-off sentiment could also depress valuations for growth stocks and companies requiring significant capital investment, as investors prioritize stability over aggressive expansion.

Broader Implications and Historical Context

The current surge in gold prices to an all-time high of $4,288 on Comex is more than just a market anomaly; it's a stark indicator of profound shifts in the global economic and political landscape. This event fits squarely into a broader trend of de-globalization and increasing geopolitical fragmentation. The escalating US-China trade war, coupled with other global uncertainties, suggests a move away from the interconnected, free-trade environment that characterized the late 20th and early 21st centuries. This trend could lead to the formation of distinct economic blocs, with supply chains re-shoring or diversifying away from traditional hubs, impacting efficiency and costs across industries.

The ripple effects extend far beyond the immediate trade dispute. Competitors and partners of the affected nations and companies will need to reassess their strategies. For instance, countries that are alternative sources of rare earth minerals or agricultural products might see increased demand, while those deeply embedded in US-China supply chains face significant disruption. Regulatory and policy implications are also vast; governments globally may be compelled to implement protectionist measures or develop new trade alliances to secure critical resources and markets. This situation could also accelerate the adoption of digital currencies or alternative financial systems as nations seek to circumvent traditional payment rails that could be weaponized in trade disputes. Historically, periods of intense geopolitical tension and economic uncertainty, such as the 1970s oil shocks or the post-9/11 era, have consistently seen gold perform strongly as a safe-haven asset, underscoring the metal's enduring role during times of crisis. The current scenario, with its unique blend of trade wars, technological rivalry, and monetary policy uncertainty, echoes these historical precedents but on an even grander, more interconnected scale.

What Comes Next: Navigating the Golden Future

Looking ahead, the trajectory of gold prices and the broader financial markets will largely hinge on the evolution of the US-China trade tensions and the global response to this escalating confrontation. In the short term, gold is likely to maintain its upward momentum as long as the trade dispute remains unresolved or intensifies. Analysts are already revising forecasts, with many projecting gold to breach the $5,000 per ounce mark by 2026. This environment presents clear opportunities for investors in gold-backed assets, including physical gold, gold ETFs, and shares of profitable gold mining companies. However, it also poses challenges for sectors vulnerable to trade disruptions, supply chain fragmentation, and reduced global demand.

Long-term possibilities suggest a more permanent recalibration of global trade and investment strategies. Companies may need to implement significant strategic pivots, such as diversifying manufacturing bases, securing alternative supply chains for critical materials like rare earths, and exploring new market opportunities outside of the traditional US-China axis. We could see a sustained period of higher commodity prices, not just for gold, but also for other essential resources, as nations prioritize resource security. Potential scenarios range from a rapid de-escalation of tensions through diplomatic breakthroughs, which could temper gold's rally, to a prolonged period of economic decoupling, which would solidify gold's role as a primary store of value. The latter scenario could also accelerate the development of regional trade blocs and foster greater economic self-sufficiency among nations. Investors should prepare for increased market volatility and the need for agile portfolio management, focusing on diversification and assets with inherent value or strong defensive characteristics.

A New Era of Uncertainty and Golden Opportunity

The historic surge of gold to $4,288 on Comex today serves as a critical marker of the current financial landscape, dominated by escalating US-China trade tensions and pervasive global uncertainty. The key takeaway is the reaffirmation of gold's role as the ultimate safe-haven asset in times of crisis, attracting massive inflows as investors abandon riskier ventures. This event is not merely a fleeting market spike but reflects deeper, structural shifts towards a more fragmented global economy and a heightened sense of geopolitical instability.

Moving forward, the market will remain highly sensitive to any developments in the US-China trade war, including tariff negotiations, technological restrictions, and diplomatic rhetoric. Investors should closely monitor economic indicators from both nations, central bank monetary policy decisions, and broader geopolitical events such as the ongoing conflict in Eastern Europe. The sustained strength of gold suggests that the market anticipates a prolonged period of uncertainty, making the precious metal a compelling component of diversified portfolios. While the immediate focus is on gold's record-breaking performance, the lasting impact will be felt across industries, compelling businesses and governments alike to adapt to a new era of strategic competition and economic realignment. Investors should watch for continued institutional demand for gold, further revisions in analyst price targets, and the performance of gold mining equities as key indicators of market sentiment in the coming months.

This content is intended for informational purposes only and is not financial advice