Broadridge has had an impressive run over the past six months. While the S&P 500 has been flat, the stock has returned 11.9% and now trades at $236.94. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is it too late to buy BR? Find out in our full research report, it’s free.

Why Does Broadridge Spark Debate?

Processing over $10 trillion in equity and fixed income trades daily and managing proxy voting for over 800 million equity positions, Broadridge Financial Solutions (NYSE: BR) provides technology-driven solutions that power investing, governance, and communications for banks, broker-dealers, asset managers, and public companies.

Two Positive Attributes:

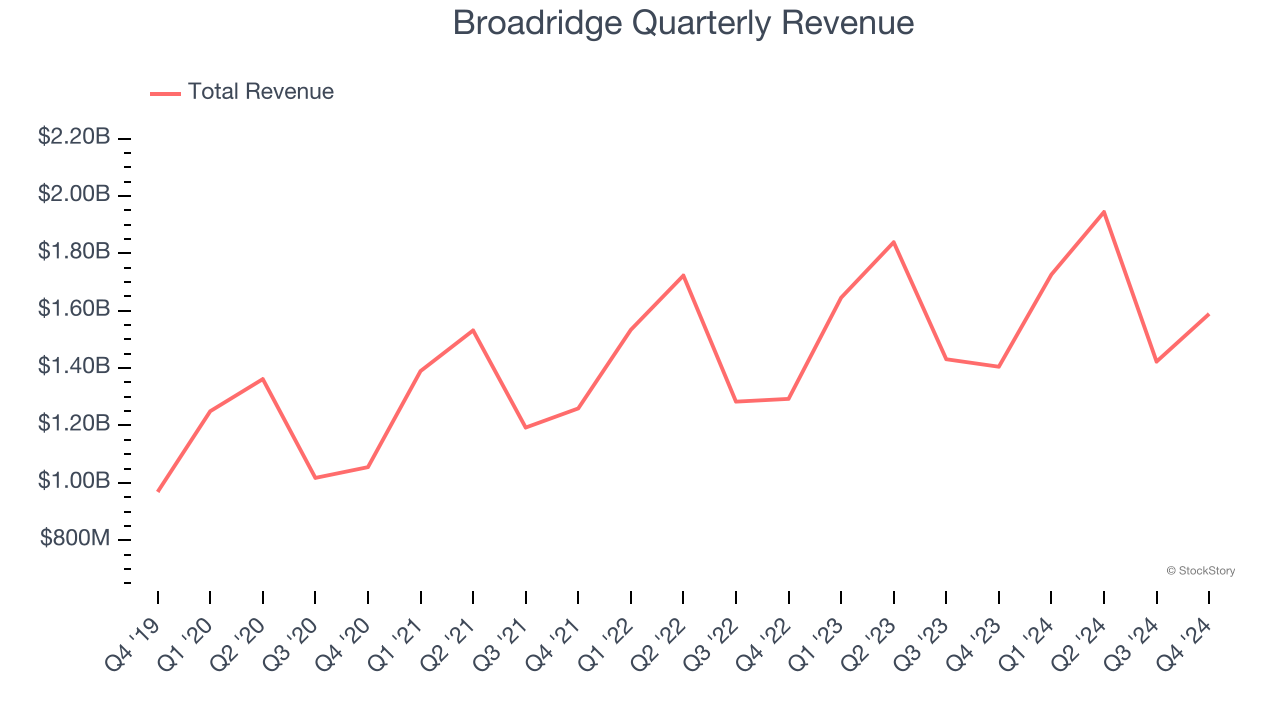

1. Long-Term Revenue Growth Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Broadridge grew its sales at a solid 9% compounded annual growth rate. Its growth surpassed the average business services company and shows its offerings resonate with customers.

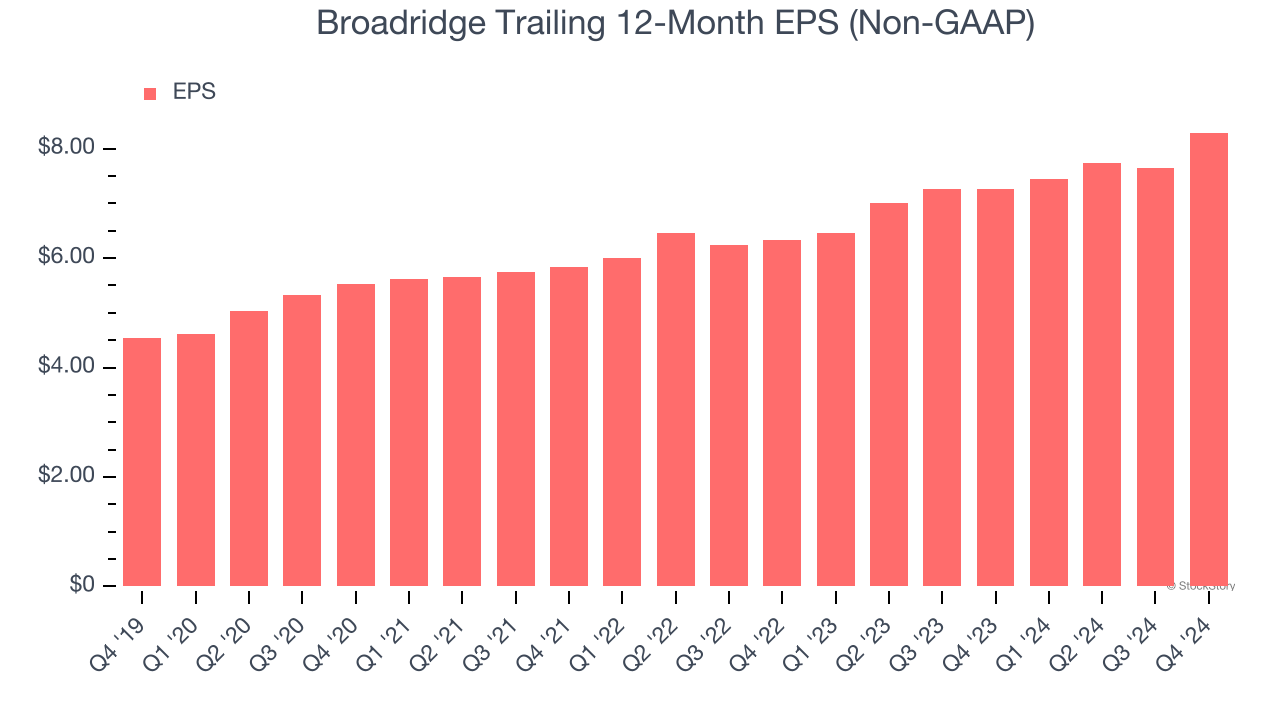

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Broadridge’s EPS grew at a spectacular 12.8% compounded annual growth rate over the last five years, higher than its 9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

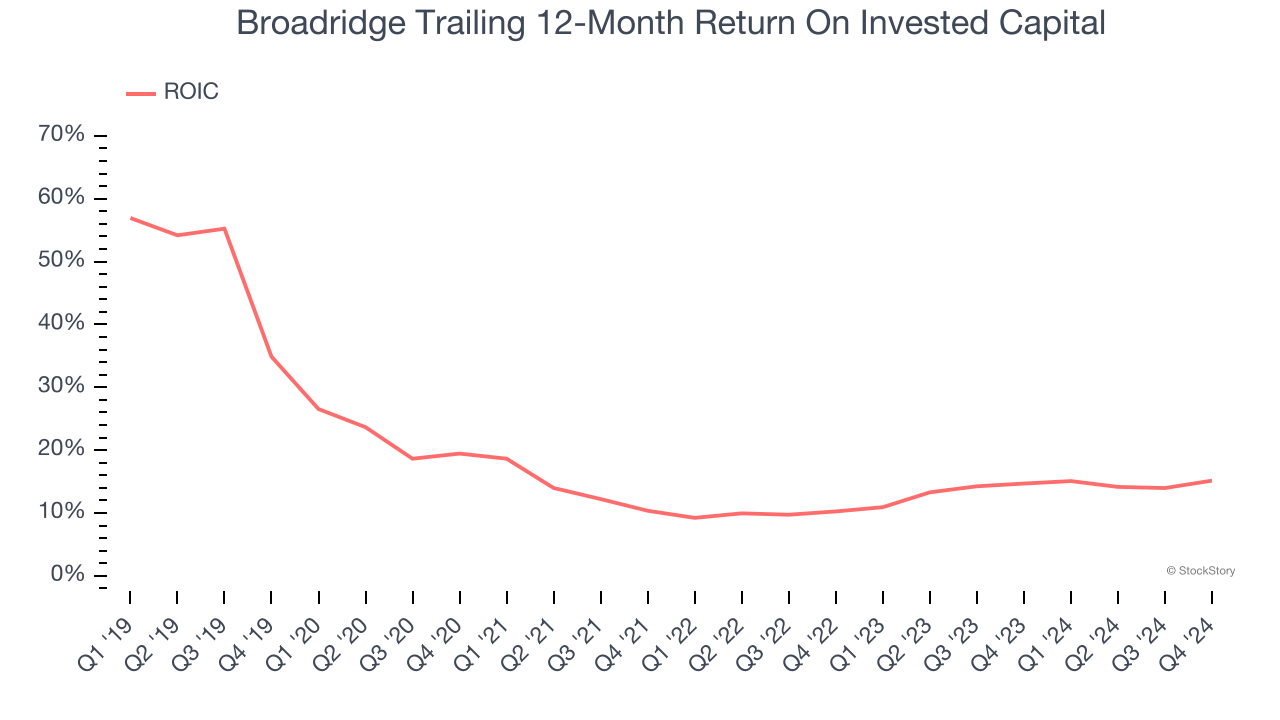

Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Broadridge has shown solid business quality lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 14%, somewhat low compared to the best business services companies that consistently pump out 25%+.

Final Judgment

Broadridge’s merits more than compensate for its flaws, and with its shares outperforming the market lately, the stock trades at 27.2× forward price-to-earnings (or $236.94 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Broadridge

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.