Shareholders of Coherent would probably like to forget the past six months even happened. The stock dropped 21.1% and now trades at $70.87. This may have investors wondering how to approach the situation.

Following the pullback, is now an opportune time to buy COHR? Find out in our full research report, it’s free.

Why Is COHR a Good Business?

Created through the 2022 rebranding of II-VI Incorporated, a company with roots dating back to 1971, Coherent (NYSE: COHR) develops and manufactures advanced materials, lasers, and optical components for applications ranging from telecommunications to industrial manufacturing.

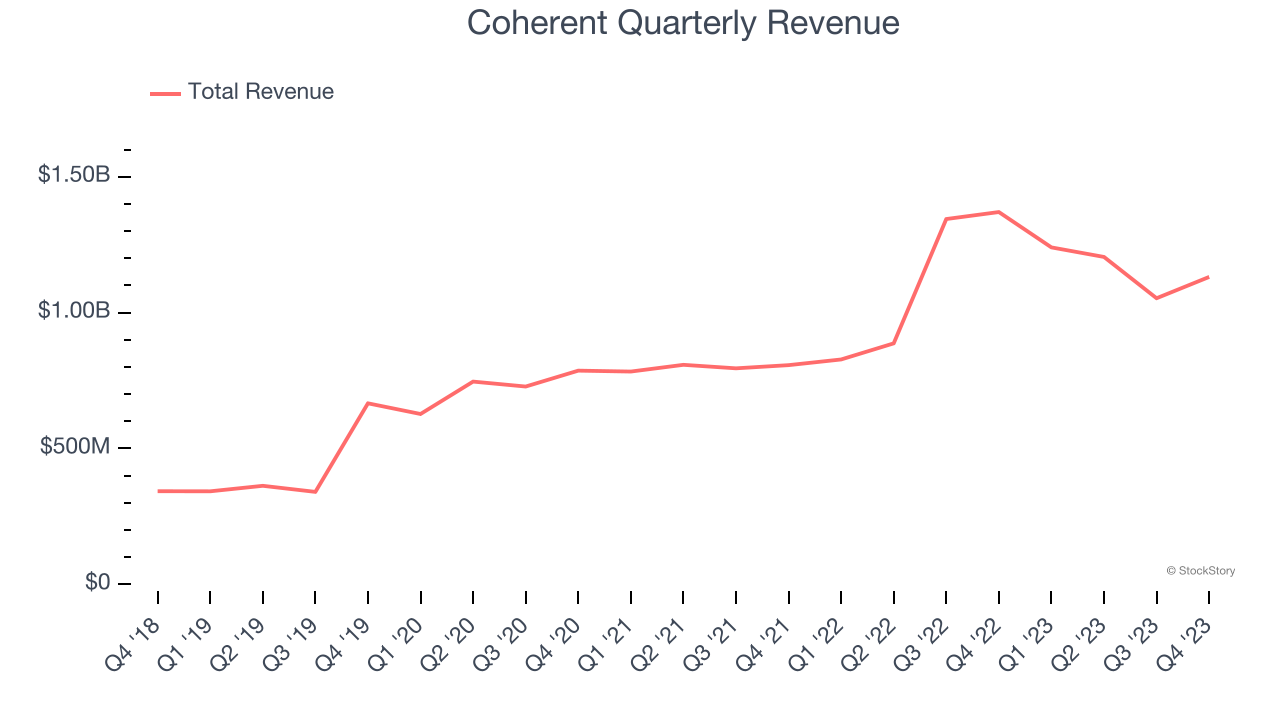

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Coherent grew its sales at an incredible 29.5% compounded annual growth rate. Its growth beat the average business services company and shows its offerings resonate with customers.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Coherent’s revenue to rise by 10.8%. While this projection is below its 20.4% annualized growth rate for the past two years, it is noteworthy and indicates the market is forecasting success for its products and services.

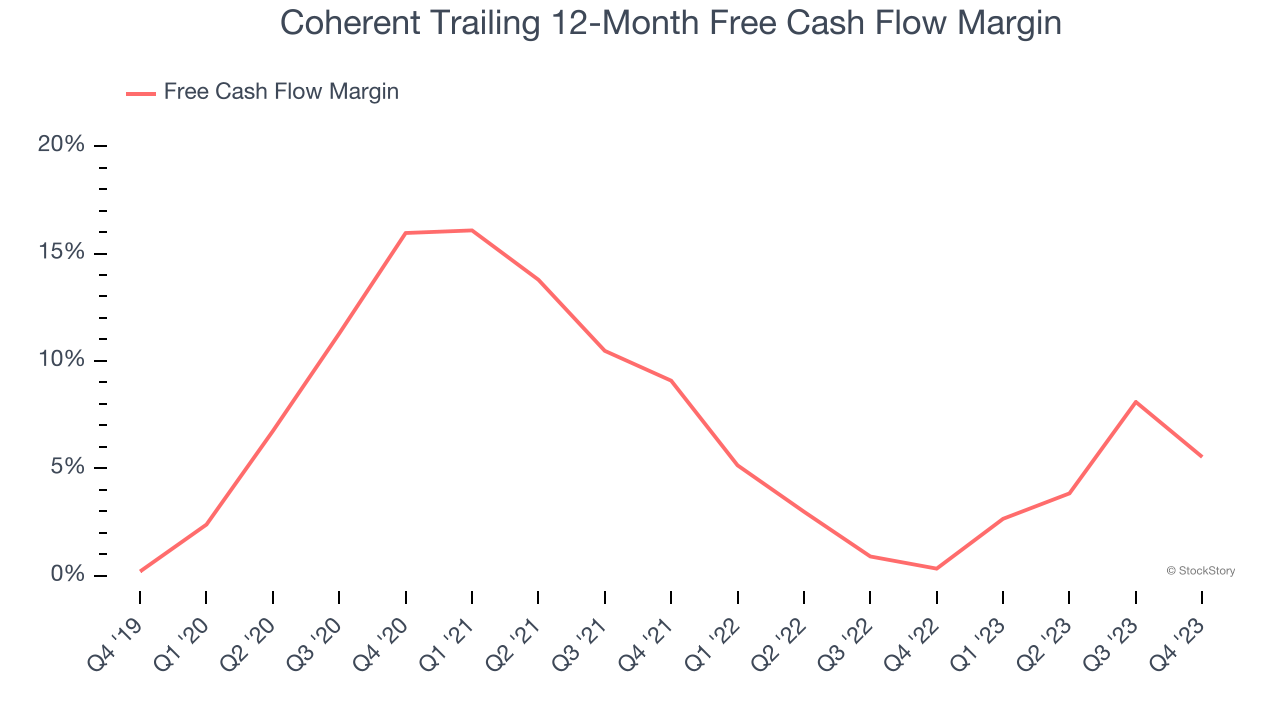

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Coherent’s margin expanded by 5.3 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Coherent’s free cash flow margin for the trailing 12 months was 5.5%.

Final Judgment

These are just a few reasons Coherent is a rock-solid business worth owning. After the recent drawdown, the stock trades at 32.6× forward price-to-earnings (or $70.87 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Coherent

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.