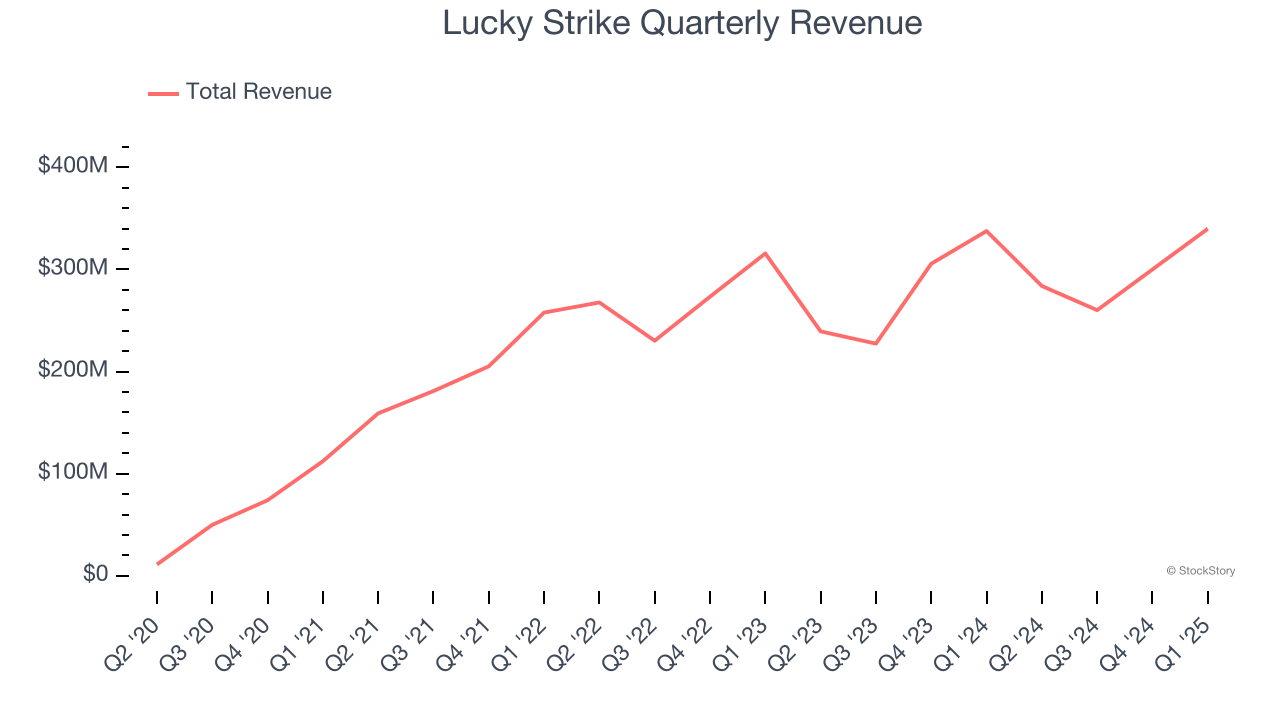

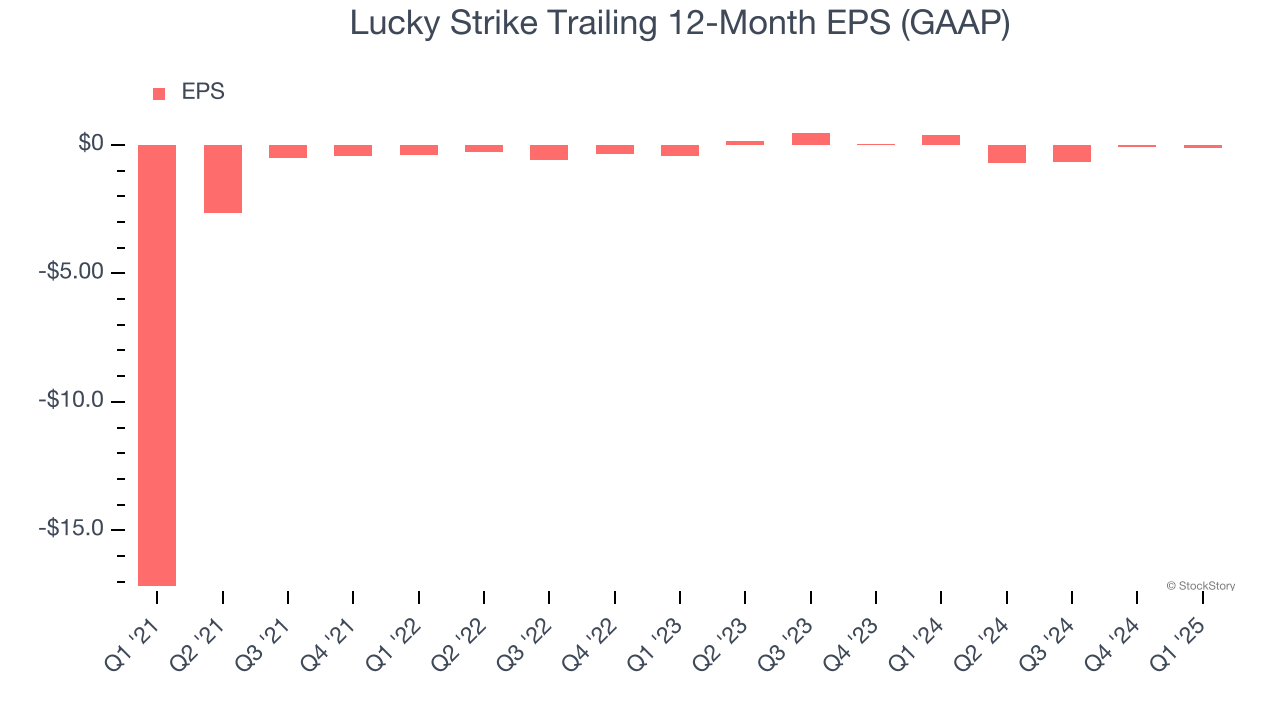

Entertainment venue operator Lucky Strike (NYSE: LUCK) fell short of the market’s revenue expectations in Q1 CY2025, with sales flat year on year at $339.9 million. Its GAAP profit of $0.07 per share was 69.6% below analysts’ consensus estimates.

Is now the time to buy Lucky Strike? Find out by accessing our full research report, it’s free.

Lucky Strike (LUCK) Q1 CY2025 Highlights:

- Revenue: $339.9 million vs analyst estimates of $359.8 million (flat year on year, 5.5% miss)

- EPS (GAAP): $0.07 vs analyst expectations of $0.23 (69.6% miss)

- Adjusted EBITDA: $117.3 million vs analyst estimates of $137.2 million (34.5% margin, 14.5% miss)

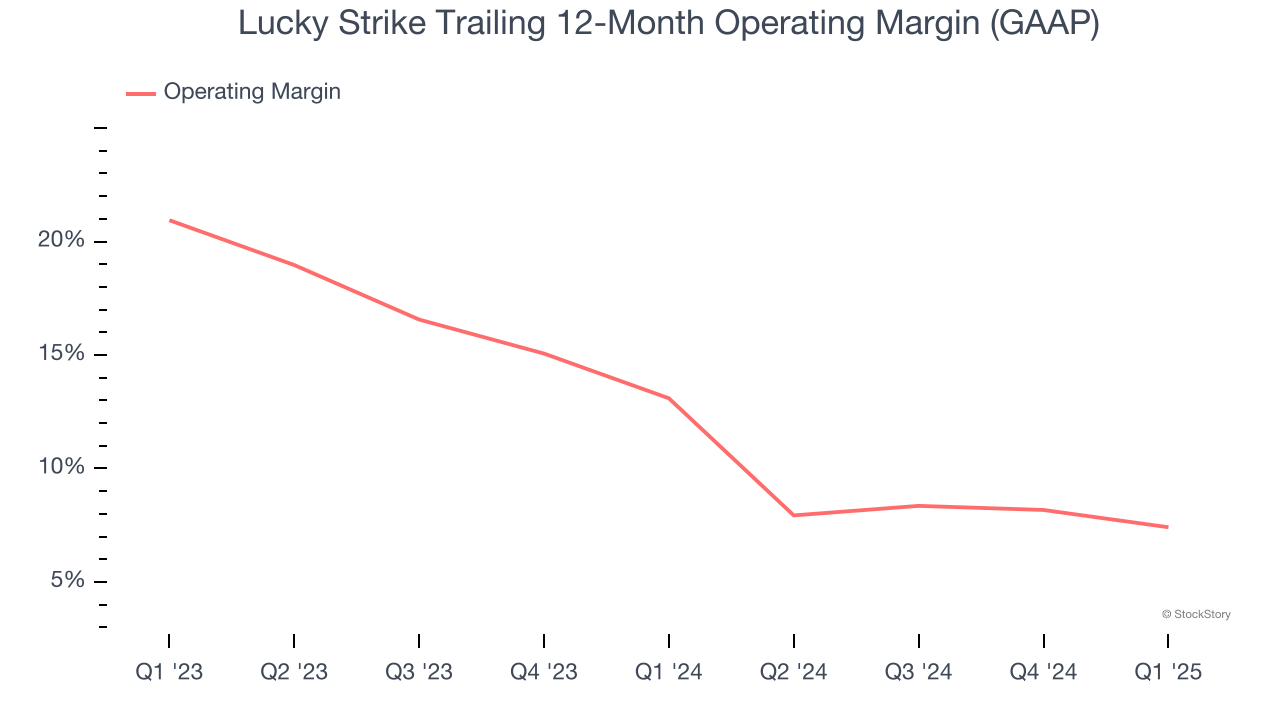

- Operating Margin: 18.3%, down from 21% in the same quarter last year

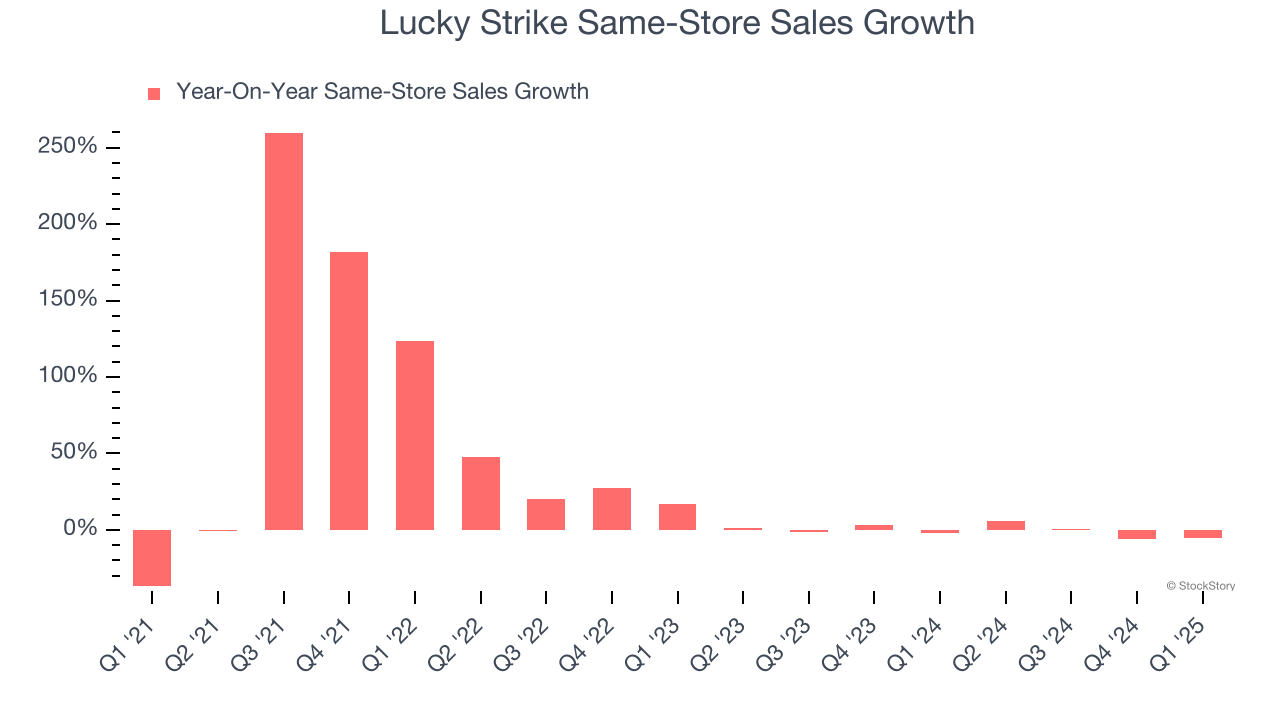

- Same-Store Sales fell 5.6% year on year (-2.1% in the same quarter last year)

- Market Capitalization: $1.37 billion

“In the quarter, our Retail and Leagues businesses remained stable, Food sales grew by high single digits, while our Corporate Events business declined as we navigate a period of corporate austerity. The softness in Corporate Events was most pronounced in tech-aligned markets, with California and Seattle accounting for the majority of the underperformance. We have seen encouraging signs of strength, with the Boston, New Jersey and Miami markets recently posting positive comps.,” said Founder, Chairman, and CEO Thomas Shannon.

Company Overview

Born from the transformation of traditional bowling alleys into modern entertainment destinations, Lucky Strike (NYSE: LUCK) operates bowling alleys and other entertainment venues with upscale amenities, arcade games, and food and beverage services across North America.

Sales Growth

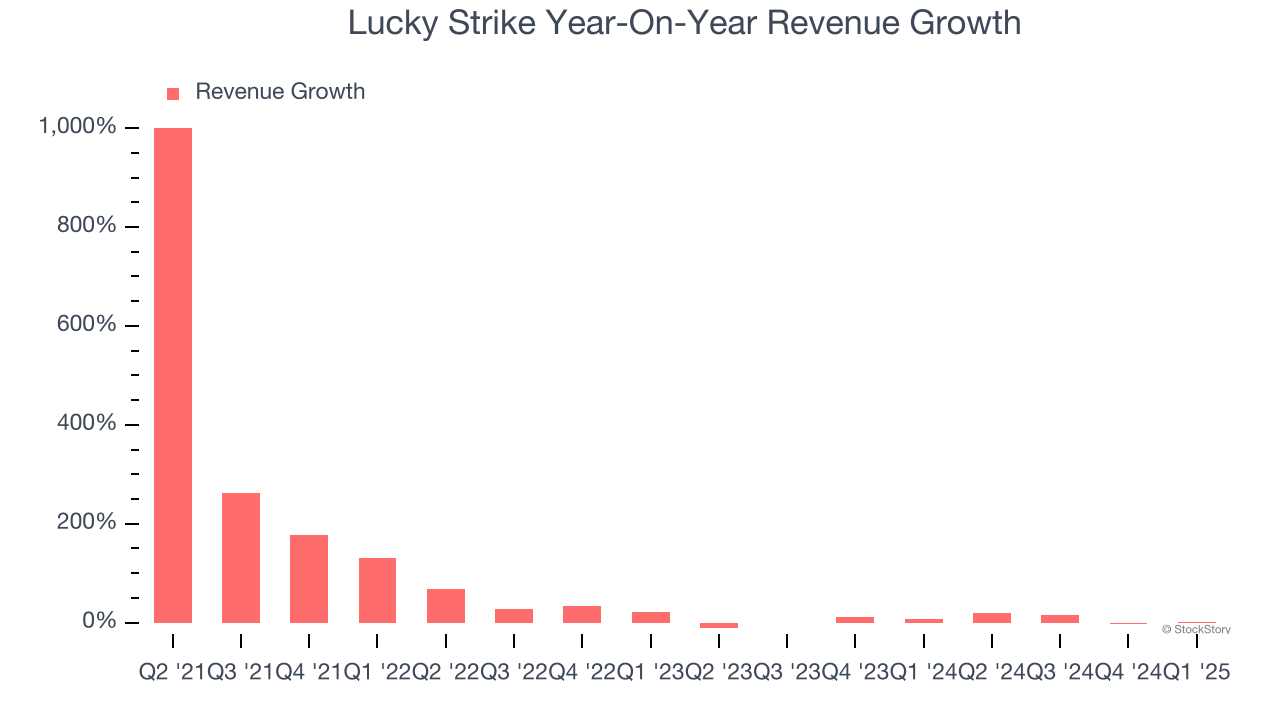

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Lucky Strike’s sales grew at an incredible 47.9% compounded annual growth rate over the last four years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Lucky Strike’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.4% over the last two years was well below its four-year trend. Note that COVID hurt Lucky Strike’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can dig further into the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Lucky Strike’s same-store sales were flat. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Lucky Strike’s $339.9 million of revenue was flat year on year, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.9% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Lucky Strike’s operating margin has shrunk over the last 12 months, but it still averaged 10.2% over the last two years, decent for a consumer discretionary business. This shows it generally does a decent job managing its expenses, and its elite historical revenue growth also suggests its margin dropped because it ramped up investments to capture market share. We’ll keep a close eye to see if this strategy pays off.

This quarter, Lucky Strike generated an operating profit margin of 18.3%, down 2.7 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Lucky Strike’s full-year earnings are still negative, it reduced its losses and improved its EPS by 71% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, Lucky Strike reported EPS at $0.07, down from $0.13 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Lucky Strike’s full-year EPS of negative $0.12 will reach break even.

Key Takeaways from Lucky Strike’s Q1 Results

We struggled to find many positives in these results. Its revenue missed significantly and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 10.8% to $8.49 immediately after reporting.

Lucky Strike underperformed this quarter, but does that create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.