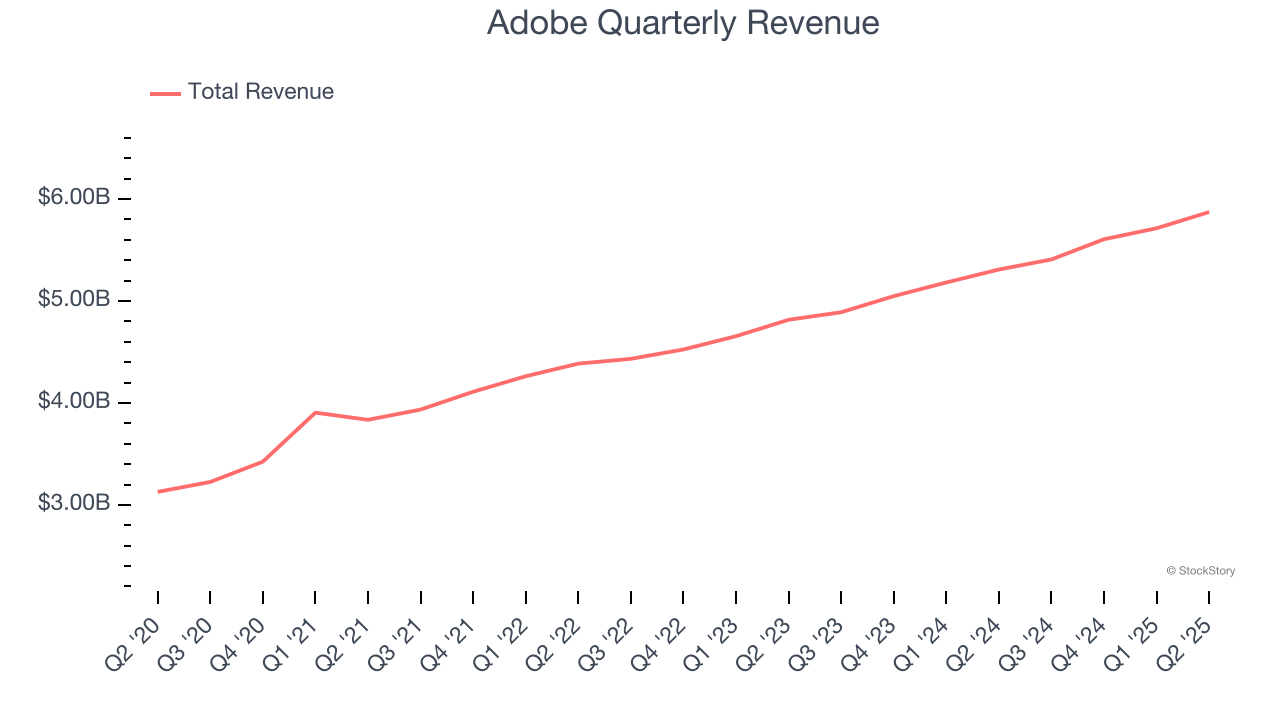

Creative software maker Adobe (NASDAQ: ADBE) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 10.6% year on year to $5.87 billion. Guidance for next quarter’s revenue was better than expected at $5.9 billion at the midpoint, 0.7% above analysts’ estimates. Its non-GAAP profit of $5.06 per share was 1.7% above analysts’ consensus estimates.

Is now the time to buy Adobe? Find out by accessing our full research report, it’s free.

Adobe (ADBE) Q2 CY2025 Highlights:

- Revenue: $5.87 billion vs analyst estimates of $5.79 billion (10.6% year-on-year growth, 1.5% beat)

- Adjusted EPS: $5.06 vs analyst estimates of $4.97 (1.7% beat)

- Adjusted Operating Income: $2.67 billion vs analyst estimates of $2.62 billion (45.5% margin, 2% beat)

- The company slightly lifted its revenue guidance for the full year to $23.55 billion at the midpoint from $23.43 billion

- Management raised its full-year Adjusted EPS guidance to $20.60 at the midpoint, a 1.2% increase

- Operating Margin: 35.9%, in line with the same quarter last year

- Free Cash Flow Margin: 36.5%, down from 43% in the previous quarter

- Annual Recurring Revenue: $18.09 billion at quarter end

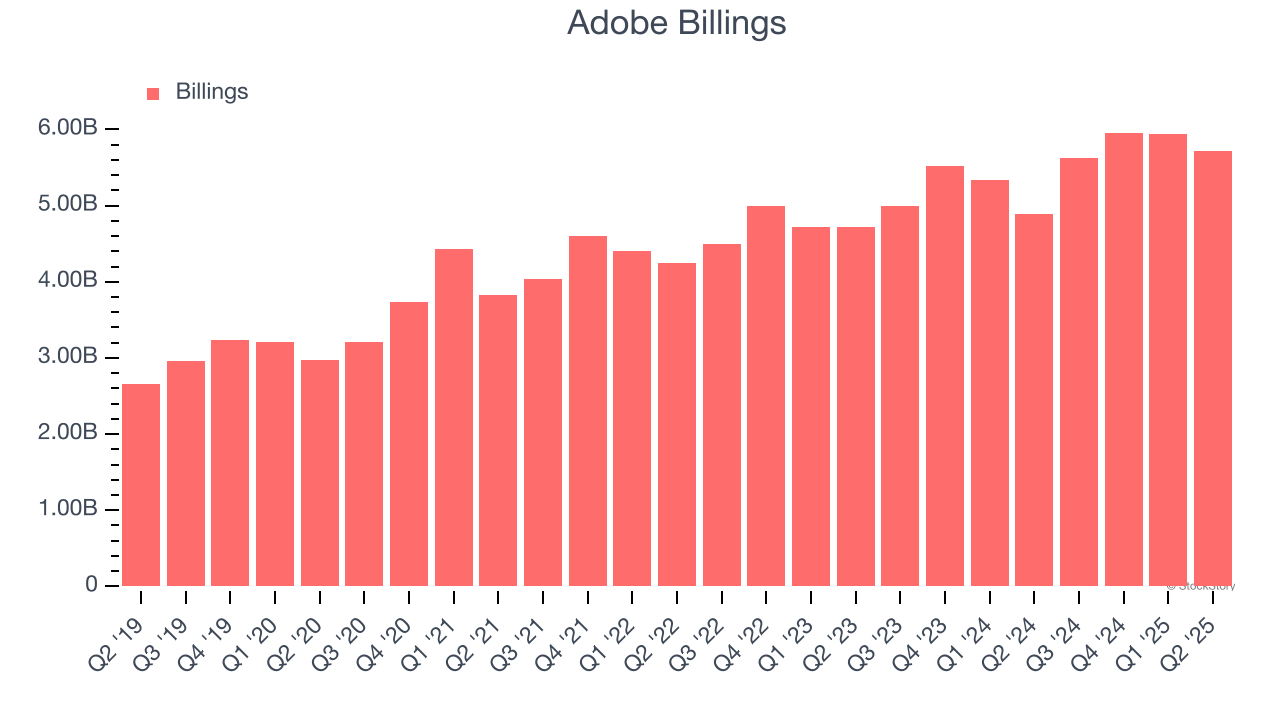

- Billings: $5.72 billion at quarter end, up 17% year on year

- Market Capitalization: $176 billion

“Our strategy to deliver ground-breaking innovation for Business Professionals and Consumers, and Creative and Marketing Professionals is delighting customers and we are pleased to raise Adobe’s FY25 revenue target,” said Shantanu Narayen, chair and CEO, Adobe.

Company Overview

One of the most well-known Silicon Valley software companies around, Adobe (NASDAQ: ADBE) is a leading provider of software as service in the digital design and document management space.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Adobe grew its sales at a 10.6% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds. Luckily, there are other things to like about Adobe.

This quarter, Adobe reported year-on-year revenue growth of 10.6%, and its $5.87 billion of revenue exceeded Wall Street’s estimates by 1.5%. Company management is currently guiding for a 9.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.2% over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Adobe’s billings punched in at $5.72 billion in Q2, and over the last four quarters, its growth slightly outpaced the sector as it averaged 12.3% year-on-year increases. This performance aligned with its total sales growth and shows the company is successfully converting sales into cash. Its growth also enhances liquidity and provides a solid foundation for future investments.

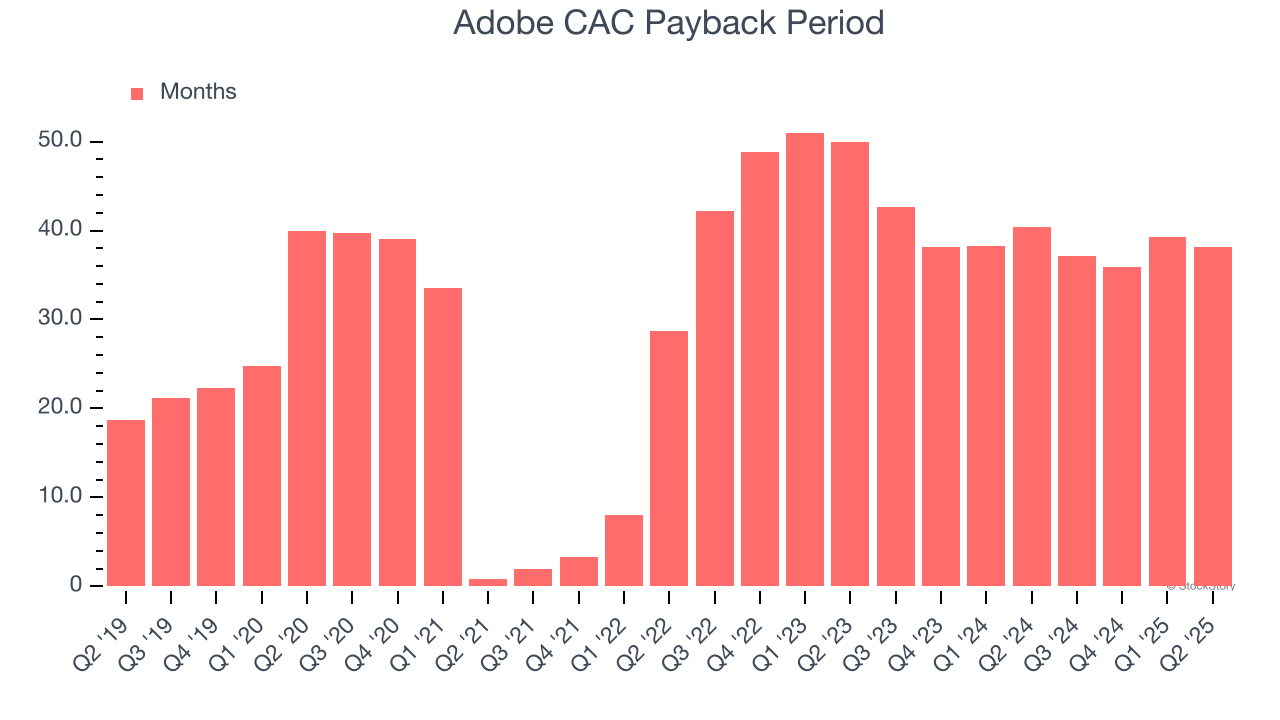

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Adobe is efficient at acquiring new customers, and its CAC payback period checked in at 38.2 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

Key Takeaways from Adobe’s Q2 Results

We enjoyed seeing Adobe beat analysts’ billings, revenue, EPS, and adjusted operating income expectations this quarter. We were also glad it lifted its full-year revenue and EPS guidance. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 1.2% to $408.88 immediately following the results.

Is Adobe an attractive investment opportunity at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.