Wrapping up Q2 earnings, we look at the numbers and key takeaways for the surgical equipment & consumables - specialty stocks, including Integra LifeSciences (NASDAQ: IART) and its peers.

The surgical equipment and consumables industry provides tools, devices, and disposable products essential for surgeries and medical procedures. These companies therefore benefit from relatively consistent demand, driven by the ongoing need for medical interventions, recurring revenue from consumables, and long-term contracts with hospitals and healthcare providers. However, the high costs of R&D and regulatory compliance, coupled with intense competition and pricing pressures from cost-conscious customers, can constrain profitability. Over the next few years, tailwinds include aging populations, which tend to need surgical interventions at higher rates. The increasing integration of AI and robotics into surgical procedures could also create opportunities for differentiation and innovation. However, the industry faces headwinds including potential supply chain vulnerabilities, evolving regulatory requirements, and more widespread efforts to make healthcare less costly.

The 4 surgical equipment & consumables - specialty stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 3.2% while next quarter’s revenue guidance was in line.

Luckily, surgical equipment & consumables - specialty stocks have performed well with share prices up 10.5% on average since the latest earnings results.

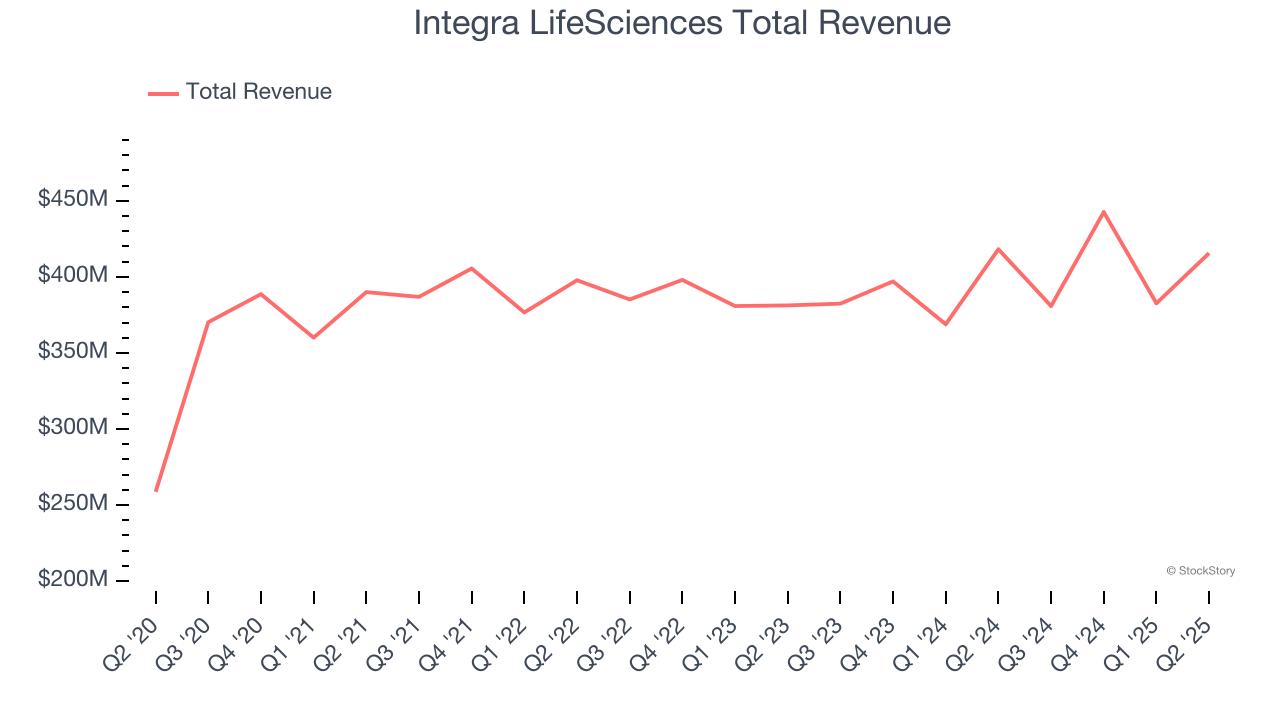

Weakest Q2: Integra LifeSciences (NASDAQ: IART)

Founded in 1989 as a pioneer in regenerative medicine technology, Integra LifeSciences (NASDAQ: IART) develops and manufactures medical technologies for neurosurgery, wound care, and surgical reconstruction, including regenerative tissue products and surgical instruments.

Integra LifeSciences reported revenues of $415.6 million, flat year on year. This print exceeded analysts’ expectations by 5.2%. Overall, it was a satisfactory quarter for the company with a solid beat of analysts’ organic revenue estimates.

“I am proud of our team’s performance and execution in the second quarter. Our strong revenue performance is a testament to our disciplined progress and the solid underlying demand trends for our portfolio of neurosurgery and tissue technology products,” said Mojdeh Poul, president and chief executive officer.

Integra LifeSciences achieved the biggest analyst estimates beat but had the slowest revenue growth and slowest revenue growth of the whole group. Unsurprisingly, the stock is up 24.7% since reporting and currently trades at $15.43.

Is now the time to buy Integra LifeSciences? Access our full analysis of the earnings results here, it’s free.

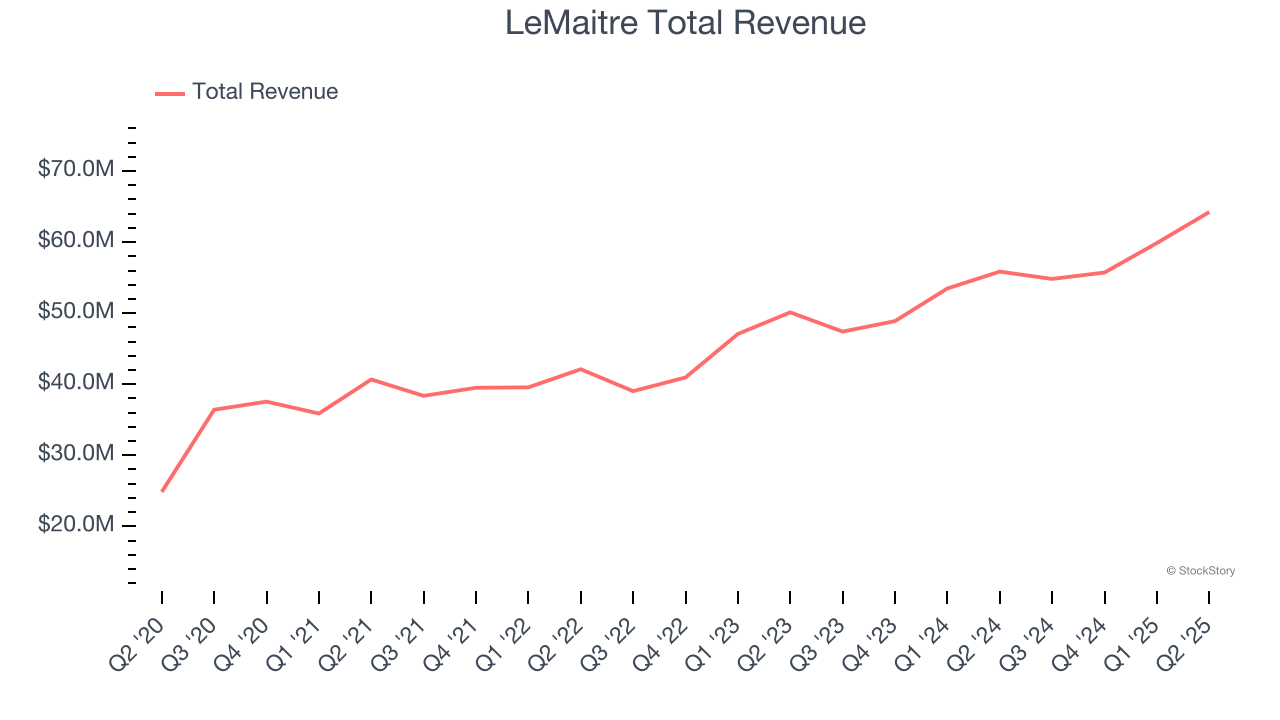

Best Q2: LeMaitre (NASDAQ: LMAT)

Founded in 1983 and named after a pioneering vascular surgeon, LeMaitre Vascular (NASDAQGM:LMAT) develops and manufactures specialized medical devices used by vascular surgeons to treat peripheral vascular disease and other circulatory conditions.

LeMaitre reported revenues of $64.23 million, up 15% year on year, outperforming analysts’ expectations by 2.6%. The business had a very strong quarter with an impressive beat of analysts’ full-year EPS guidance estimates and an impressive beat of analysts’ organic revenue estimates.

LeMaitre delivered the highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 11.3% since reporting. It currently trades at $95.68.

Is now the time to buy LeMaitre? Access our full analysis of the earnings results here, it’s free.

Intuitive Surgical (NASDAQ: ISRG)

Pioneering minimally invasive surgery since its first da Vinci system was FDA-cleared in 2000, Intuitive Surgical (NASDAQ: ISRG) develops and manufactures robotic-assisted surgical systems that enable minimally invasive procedures across various medical specialties.

Intuitive Surgical reported revenues of $2.44 billion, up 21.4% year on year, exceeding analysts’ expectations by 3.7%. It may have had the worst quarter among its peers, but its results were still good as it also locked in a beat of analysts’ EPS estimates.

As expected, the stock is down 7.7% since the results and currently trades at $472.

Read our full analysis of Intuitive Surgical’s results here.

Teleflex (NYSE: TFX)

With a portfolio spanning from vascular access catheters to minimally invasive surgical tools, Teleflex (NYSE: TFX) designs, manufactures, and supplies single-use medical devices used in critical care and surgical procedures across hospitals worldwide.

Teleflex reported revenues of $780.9 million, up 2.3% year on year. This print topped analysts’ expectations by 1.3%. It was a very strong quarter as it also produced a solid beat of analysts’ full-year EPS guidance estimates and a beat of analysts’ EPS estimates.

Teleflex had the weakest performance against analyst estimates among its peers. The stock is up 13.7% since reporting and currently trades at $129.50.

Read our full, actionable report on Teleflex here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.