Let’s dig into the relative performance of IMAX (NYSE: IMAX) and its peers as we unravel the now-completed Q3 traditional media & publishing earnings season.

The sector faces structural headwinds from declining linear TV viewership, shifts in advertising spend toward digital platforms, and ongoing challenges in monetizing print and broadcast content. However, for companies that invest wisely, tailwinds can include AI, the power of which can result in more personalized content creation and more detailed audience analysis. These can create a flywheel of success where one feeds into the other. Still there are outstanding questions around AI-generated content oversight, and the regulatory framework around this could evolve in unseen ways over the next few years.

The 4 traditional media & publishing stocks we track reported a very strong Q3. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 0.8% below.

Luckily, traditional media & publishing stocks have performed well with share prices up 14.8% on average since the latest earnings results.

IMAX (NYSE: IMAX)

Originally developed for World Expo '67 in Montreal as an innovative projection system, IMAX (NYSE: IMAX) provides proprietary large-format cinema technology and systems that deliver immersive movie experiences with enhanced image quality and sound.

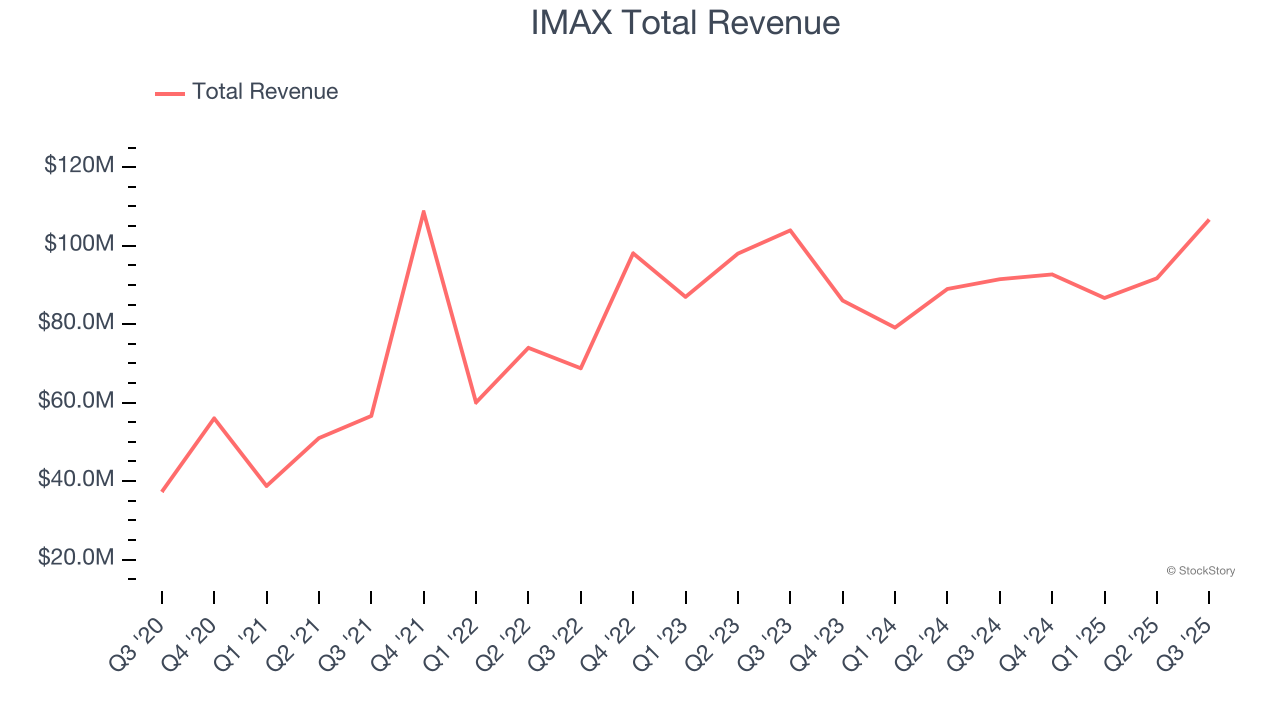

IMAX reported revenues of $106.7 million, up 16.6% year on year. This print exceeded analysts’ expectations by 0.6%. Overall, it was an exceptional quarter for the company with a beat of analysts’ EPS estimates and a narrow beat of analysts’ revenue estimates.

“IMAX is moving into a new position — building to something bigger — and our performance for the quarter and year to date demonstrate we’re breaking out and delivering at a higher level,” said Rich Gelfond, CEO of IMAX.

IMAX achieved the fastest revenue growth of the whole group. Unsurprisingly, the stock is up 15.4% since reporting and currently trades at $37.

Is now the time to buy IMAX? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Sinclair (NASDAQ: SBGI)

With over 2,400 hours of local news produced weekly and 640 broadcast channels reaching millions of American homes, Sinclair (NASDAQ: SBGI) operates a network of 185 local television stations across 86 U.S. markets, producing news programming and distributing content from major networks.

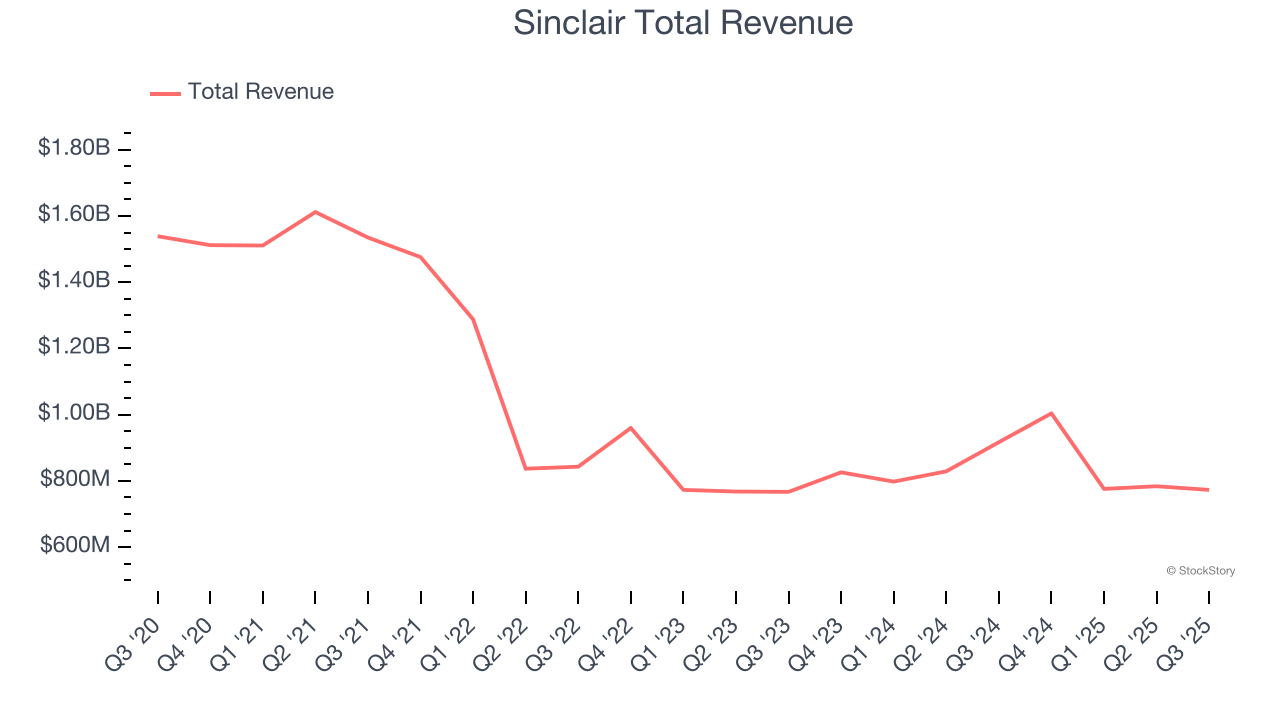

Sinclair reported revenues of $773 million, down 15.7% year on year, outperforming analysts’ expectations by 0.6%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and full-year revenue guidance exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 12.3% since reporting. It currently trades at $15.30.

Is now the time to buy Sinclair? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: EchoStar (NASDAQ: SATS)

Following its 2023 acquisition of DISH Network, EchoStar (NASDAQ: SATS) provides satellite communications, pay-TV services, wireless networks, and broadband solutions across consumer and enterprise markets.

EchoStar reported revenues of $3.61 billion, down 7.1% year on year, falling short of analysts’ expectations by 3.1%. It was a slower quarter as it posted a significant miss of analysts’ revenue estimates.

EchoStar delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 50.6% since the results and currently trades at $108.93.

Read our full analysis of EchoStar’s results here.

Wiley (NYSE: WLY)

With roots dating back to 1807 when Charles Wiley opened a small printing shop in Manhattan, John Wiley & Sons (NYSE: WLY) is a global academic publisher that provides scientific journals, books, digital courseware, and knowledge solutions for researchers, students, and professionals.

Wiley reported revenues of $421.8 million, down 1.1% year on year. This result beat analysts’ expectations by 1.3%. It was an exceptional quarter as it also logged a beat of analysts’ EPS estimates and an impressive beat of analysts’ full-year EPS guidance estimates.

Wiley scored the biggest analyst estimates beat among its peers. The stock is down 19.2% since reporting and currently trades at $30.63.

Read our full, actionable report on Wiley here, it’s free for active Edge members.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.