Curtiss-Wright currently trades at $587.76 and has been a dream stock for shareholders. It’s returned 400% since January 2021, blowing past the S&P 500’s 81.4% gain. The company has also beaten the index over the past six months as its stock price is up 19.6% thanks to its solid quarterly results.

Is it too late to buy CW? Find out in our full research report, it’s free for active Edge members.

Why Are We Positive On Curtiss-Wright?

Formed from a merger of 12 companies, Curtiss-Wright (NYSE: CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

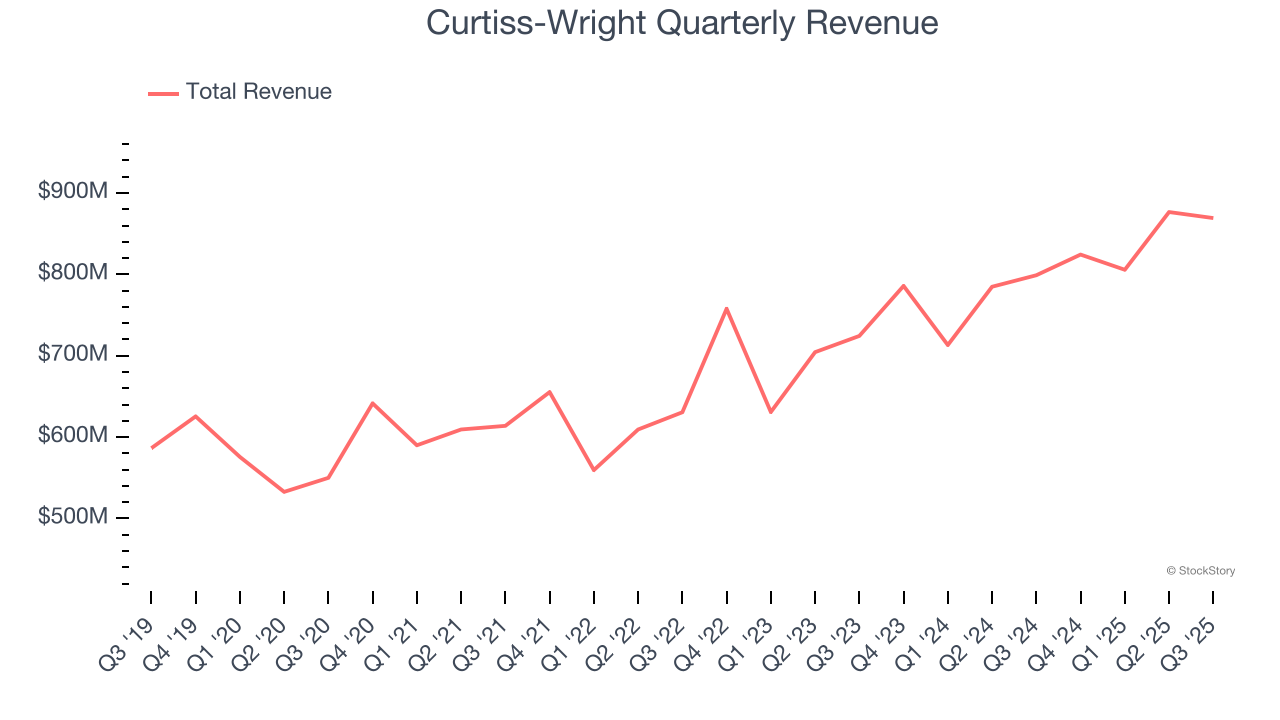

1. Long-Term Revenue Growth Shows Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Curtiss-Wright’s sales grew at a decent 8.1% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

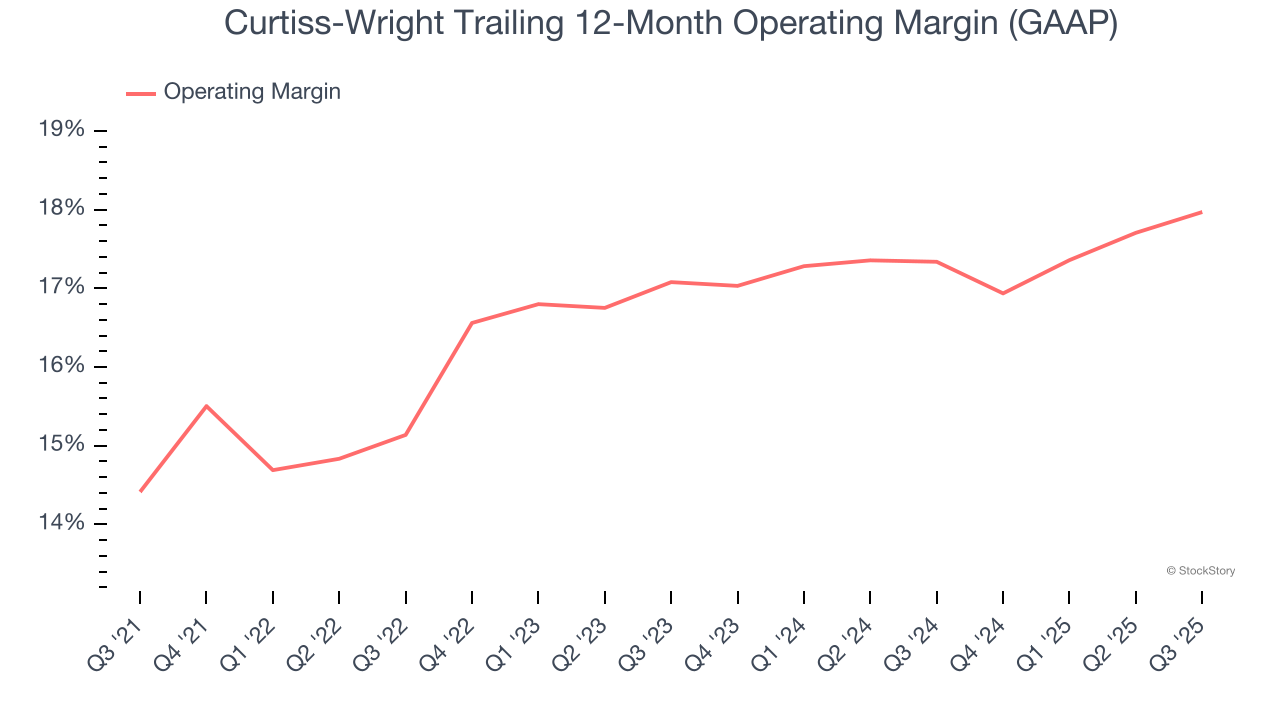

2. Operating Margin Reveals a Well-Run Organization

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Curtiss-Wright has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.5%.

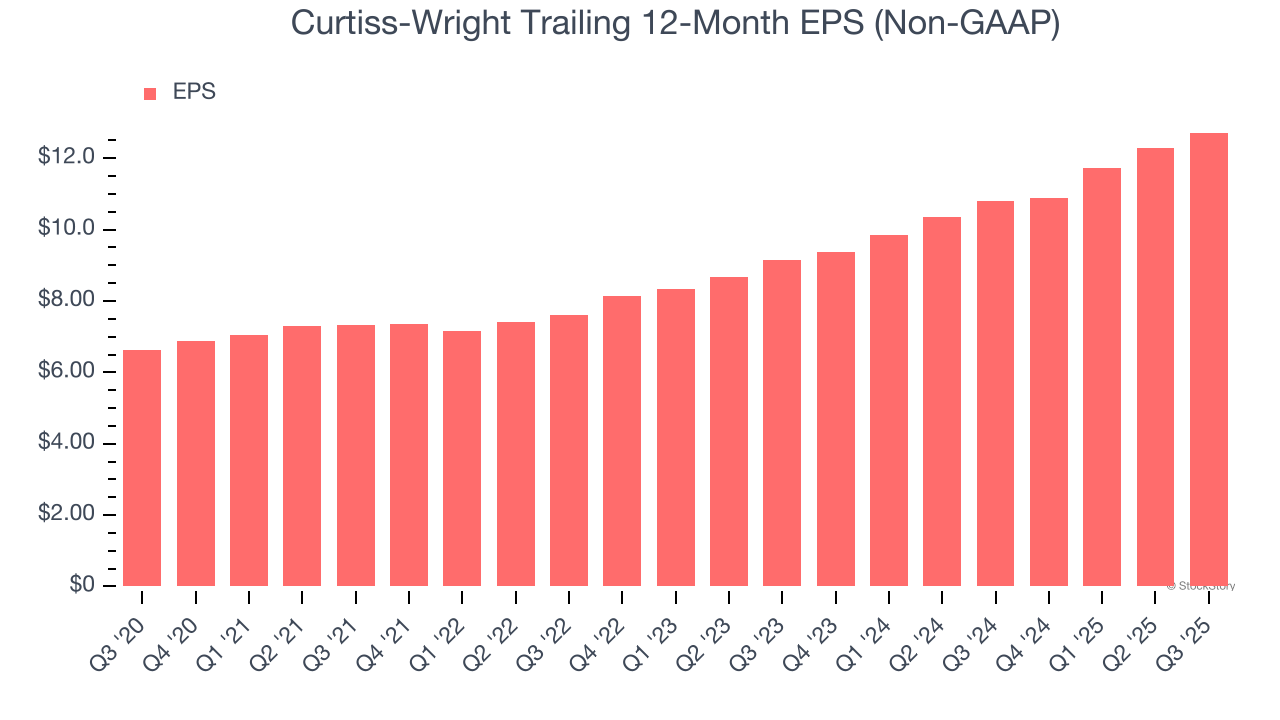

3. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Curtiss-Wright’s EPS grew at a remarkable 14% compounded annual growth rate over the last five years, higher than its 8.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we think Curtiss-Wright is a great business, and with its shares topping the market in recent months, the stock trades at 41.8× forward P/E (or $587.76 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free for active Edge members.

Stocks We Like Even More Than Curtiss-Wright

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.